DDA Crypto Market Pulse, March 20, 2023

by André Dragosch, Head of Research

Key Takeaways

- Cryptoassets are feasting on a likely pause in the Fed rate hiking cycle and final Fed easing cycle due to the current stress in the banking sector

- Our in-house Crypto Sentiment Index has significantly recovered compared to last week and is now neutral again

- There has also been a significant underperformance of Ethereum versus Bitcoin which appears to be mostly due to on-chain factors

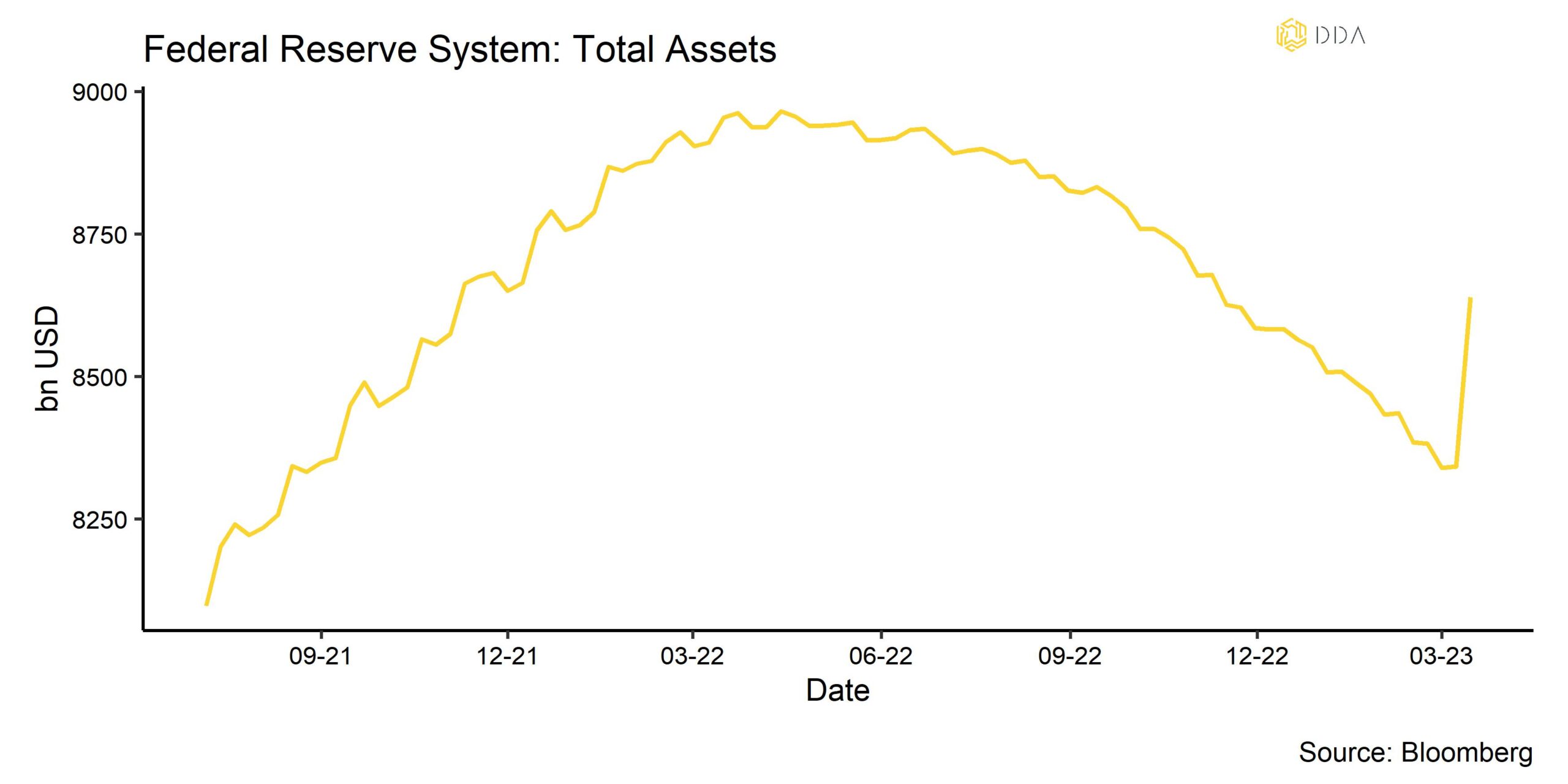

Chart of the week

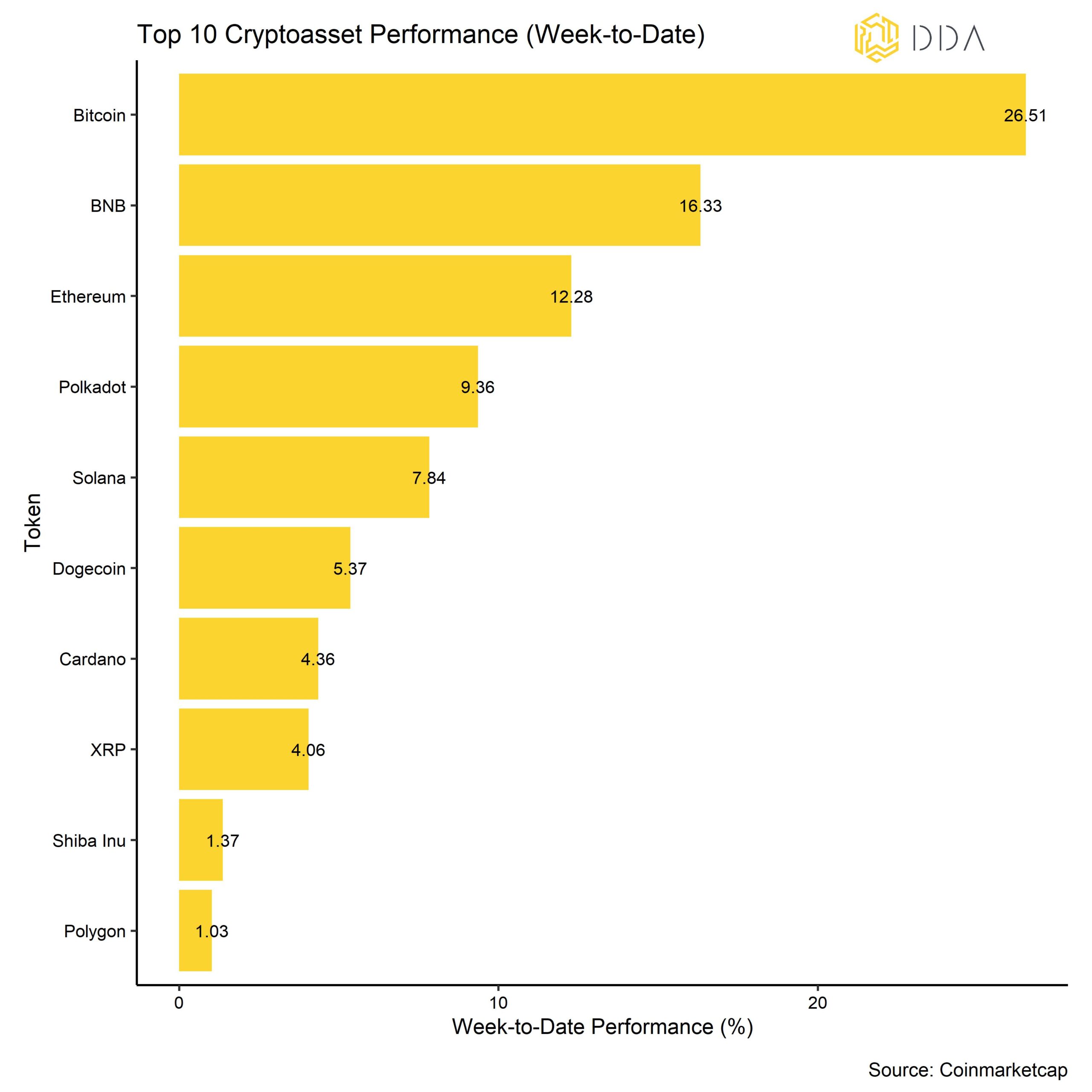

Cryptoasset Performance

Last week’s cryptoasset performances were one of the strongest since early-2021, ie during the last bull market. This was mostly due to an anticipated pause in the Fed hiking cycle and final Fed easing cycle due to the current stress in the banking sector.

Markets were particularly feasting on the fact that the total assets of the Federal Reserve have increased by ~300 bn USD in a single week (see Chart-of-the-Week). Although many market observers have been cautious to call this another round of “Quantitative Easing” (QE) by the Fed, there has also been a significant increase in commercial bank reserves at the Fed (~250 bn USD) which represents a net liquidity increase in the US interbank market and therefore de facto easing of liquidity conditions by the Fed. We have also seen the biggest use of the Fed’s discount window (~156 bn USD) since the Covid-crisis which also highlights the significant liquidity provision by the Fed in light of the stress in the banking sector.

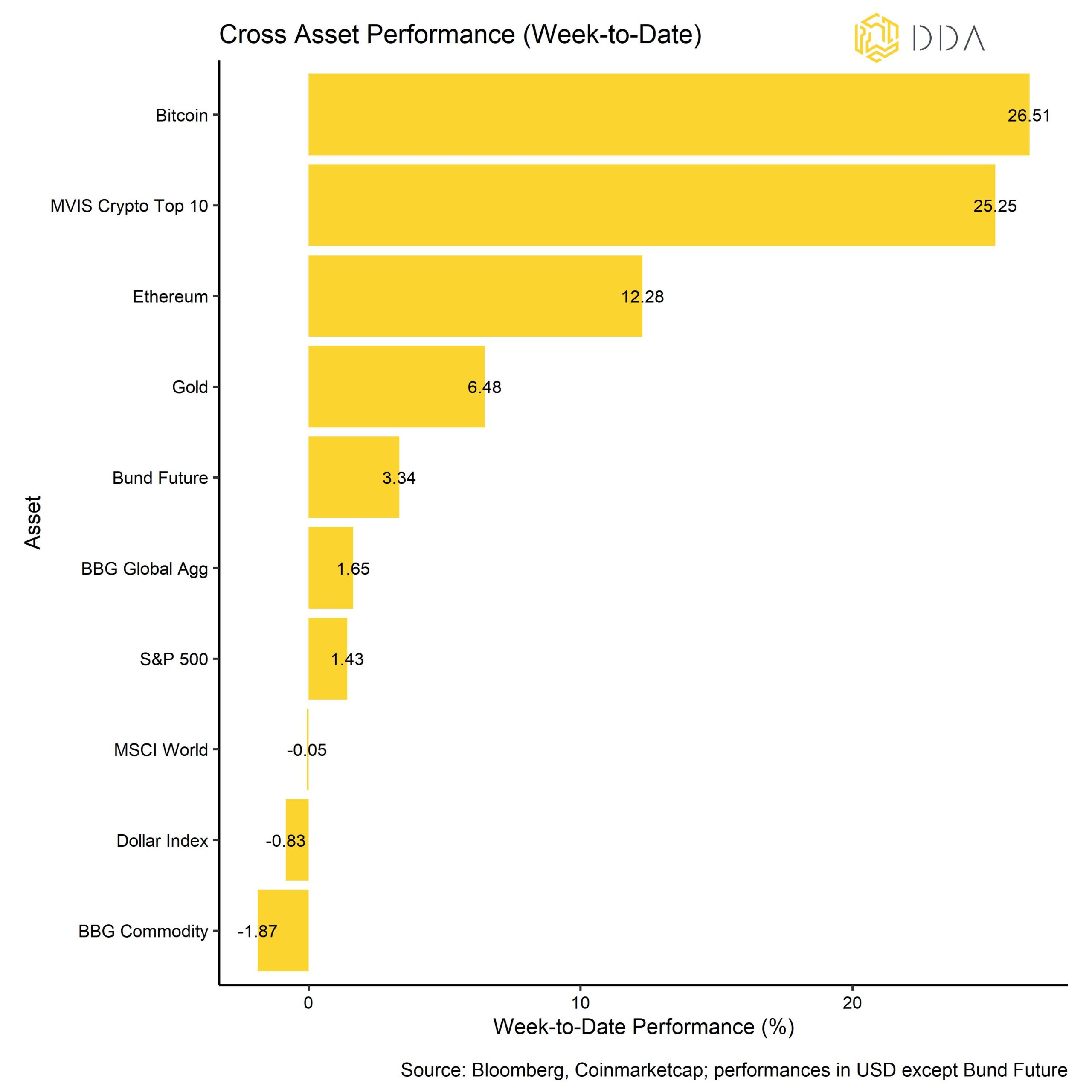

Although cryptoassets outperformed by a very wide margin, other traditional financial assets such as stocks, bonds and gold performed relatively-well also due to the outlook for further Fed easing in monetary policy. Only the Dollar and commodities were weighed down by the prospects of an increase in liquidity and the higher probability of a recession.

Among the major cryptoassets, Bitcoin, BNB, and Ethereum were the relative outperformers. However, there was a significant underperformance of Ethereum vs Bitcoin (ETH/BTC) due to an increase in “voluntary exit count” ahead of the Shanghai Upgrade. (More on that in the on-chain section below).

Crypto Market Sentiment

Our in-house Crypto Sentiment Index has significantly reversed compared to last week and is now in neutral territory again. 8 out of 15 indicators are above their short-term trend.

Compared to last week, we saw major reversals in the BTC short-term holder Spent-Output-Profit-Ratio (STH-SOPR) and 1-month 25-delta option skew.

The Crypto Fear & Greed Index increased significantly above the 50%-line into “Greed” territory.

Dispersion among cryptoassets continued to be low as most cryptoassets were increasingly trading on systematic factors. At the same time, altcoins also underperformed Bitcoin on a 1-month and 3-months basis. On a 1-month basis, only 20% of tracked altcoins have managed to outperform Bitcoin. Altcoin outperformance is usually a sign of increased risk appetite and low altcoin outperformance is still indicative of a rather cautious market sentiment.

Crypto Asset Flows

Last week was another week with very significant fund outflows from cryptoassets, despite very strong performances in the asset class. Investors generally appear to be in need of liquidity due to the current stress in banking sector which could explain these kind of fund flow developments.

In aggregate, we saw net fund outflows in the amount of -172.5 mn USD. All types of products experienced net outflows with the exception of Altcoin funds (+1.0 mn USD). Fund outflows were heavily concentrated in Bitcoin funds (-102.8 mn USD) and Ethereum funds (-42.5 mn USD) while Basket & Thematic crypto funds also experienced significant net outflows (-28.3 mn USD).

In contrast, the NAV discount of the biggest Bitcoin fund in the world – Grayscale Bitcoin Trust (GBTC) – has managed to narrow a bit which implies net inflows into this fund vehicle.

Compared to last week, the beta of global Hedge Funds to Bitcoin over the last 20 trading days continued to decrease and is now below 0, implying that global hedge funds now have a net short position in cryptoassets.

Bitcoin prices traded on Coinbase vis-à-vis those traded on Binance (Coinbase-Binance premium) were positive throughout the week, which is indicative of increased buying interest from institutional investors vis-à-vis retail investors in face of the market ructions.

On-Chain Activity

On-Chain activity was consistent with an increase in overall risk aversion in crypto markets as exchange inflows have generally picked up in light of the increased uncertainty.

More specifically, we have seen the highest amount of Bitcoin exchange inflows since the FTX fall-out in November 2022. Contrary to the current price action, we have seen a continuous increase in BTC exchange balances. Meanwhile, ETH exchange balances continued to trend lower.

In addition, we have also seen continuously high exchange transfers from BTC miner wallets to exchanges implying that the combination of relatively low prices and high hash rate is still weighing on Bitcoin miners’ financials. The large majority of these transfer appear to be coming from the Poolin BTC mining pool. In this context, BTC hash rate has continued to stay near all-time high levels.

Concerning the recent underperformance of Ethereum vs Bitcoin (ETH/BTC), there appears to be an increase in uncertainty concerning the upcoming Shanghai-Capella Upgrade, also known as Shapella.

The Ethereum Improvement Proposal (EIP) 4895, which will allow validator staking withdrawals on the main network, is the upgrade’s standout. This crucial feature was left out when Ethereum switched to proof-of-stake (PoS) consensus following the Merge upgrade in September 2022.

We have recently seen an increase in “voluntary exit count” on the Ethereum blockchain to the highest level since September 2022, and the second highest ever.

The voluntary exit count represents the total number of validators who voluntarily left the validator pool.

A validator enters the exit queue when they decide to stop taking part in consensus. Although these validators no longer propose or testify to blocks, the ETH stake is still present and cannot be removed just yet. This has increased uncertainty ahead of the Shapella upgrade.

Moreover, fees on Ethereum have increased significantly along with the increase in the price in USD which currently weighs on the perceived utility of the L1-chain. At one point, median fees on the Ethereum main net had increase to the highest level since May 2022.

Most market observers account the recent ETH/BTC underperformance to these on-chain developments.

Cryptoasset Derivatives

In general, we have seen an overall increase in implied volatilities due to the sharp reversal and increase in prices last week. This is mostly due to an increase in upside price volatility which can also be seen in the increase in 1-month 25-delta option skew of Bitcoin that has also reversed into positive territory again. That implies that option traders are paying up for delta-equivalent call options vis-à-vis put options.

Moreover, there was a very significant reversal in both the futures basis rate and perpetual funding rates which imply a winding down in short positions in Bitcoin due to the sharp increase in price. However, there has not been a significant increase in short futures liquidations which implies that most of that re-positioning in futures and perpetual contracts was done voluntarily.

Bottom Line

Cryptoassets are feasting on a likely pause in the Fed rate hiking cycle and final Fed easing cycle due to the current stress in the banking sector.

Our in-house Crypto Sentiment Index has significantly recovered compared to last week and is now neutral again.

There has also been a significant underperformance of Ethereum versus Bitcoin which appears to be mostly due to on-chain factors.

About Deutsche Digital Assets

Deutsche Digital Assets is the trusted one-stop-shop for investors seeking exposure to crypto assets. We offer a menu of crypto investment products and solutions, ranging from passive to actively managed exposure, as well as financial product white-labeling services for asset managers.

We deliver excellence through familiar, trusted investment vehicles, providing investors the quality assurances they deserve from a world-class asset manager as we champion our mission of driving crypto asset adoption. DDA removes the technical risks of crypto investing by offering investors trusted and familiar means to invest in crypto at industry-leading low costs.

Legal Disclaimer

The material and information contained in this article is for informational purposes only. Deutsche Digital Assets, its affiliates, and subsidiaries are not soliciting any action based upon such material. This article is neither investment advice nor a recommendation or solicitation to buy any securities. Performance is unpredictable. Past performance is hence not an indication of any future performance. You agree to do your own research and due diligence before making any investment decision with respect to securities or investment opportunities discussed herein. Our articles and reports include forward-looking statements, estimates, projections, and opinions. These may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond Deutsche Digital Assets GmbH’s control. We believe all information contained herein is accurate, reliable and has been obtained from public sources. However, such information is presented “as is” without warranty of any kind.