DDA Crypto Market Pulse, April 17, 2023

by André Dragosch, Head of Research

Key Takeaways

- The successful Ethereum Shapella upgrade as well as disappointing US macro data have led to just another upleg in cryptoasset prices

- Despite the recent price increases, our in-house Crypto Sentiment Index still remains neutral which signals no short-term exuberance so far

- Derivatives developments both for Bitcoin and Ethereum appear to be at the forefront of the recent price move once again as traders were generally busy unwinding their hedges after the upgrade

Chart of the week

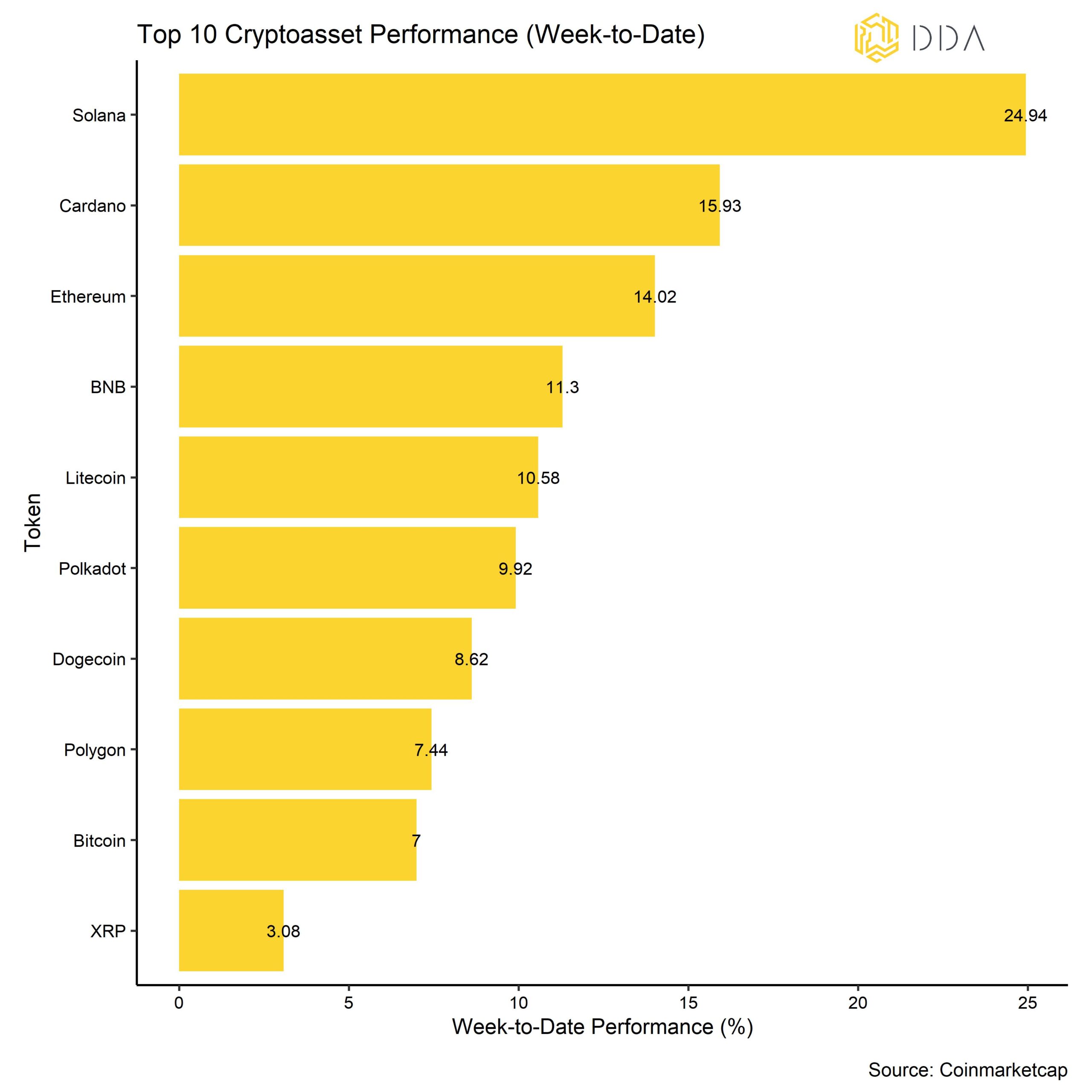

Cryptoasset Performance

Last week’s cryptoasset performances were propped up by both positive on-chain and macro factors. On the one hand, weaker than expected US inflation data and higher unemployment claims led to a further pricing out of tight US monetary policy and lower yields that weakened the US Dollar. On the other hand, the successful Ethereum Shapella upgrade led to a broad decrease in risk aversion in cryptoasset markets last week and contributed to an overall positive risk sentiment.

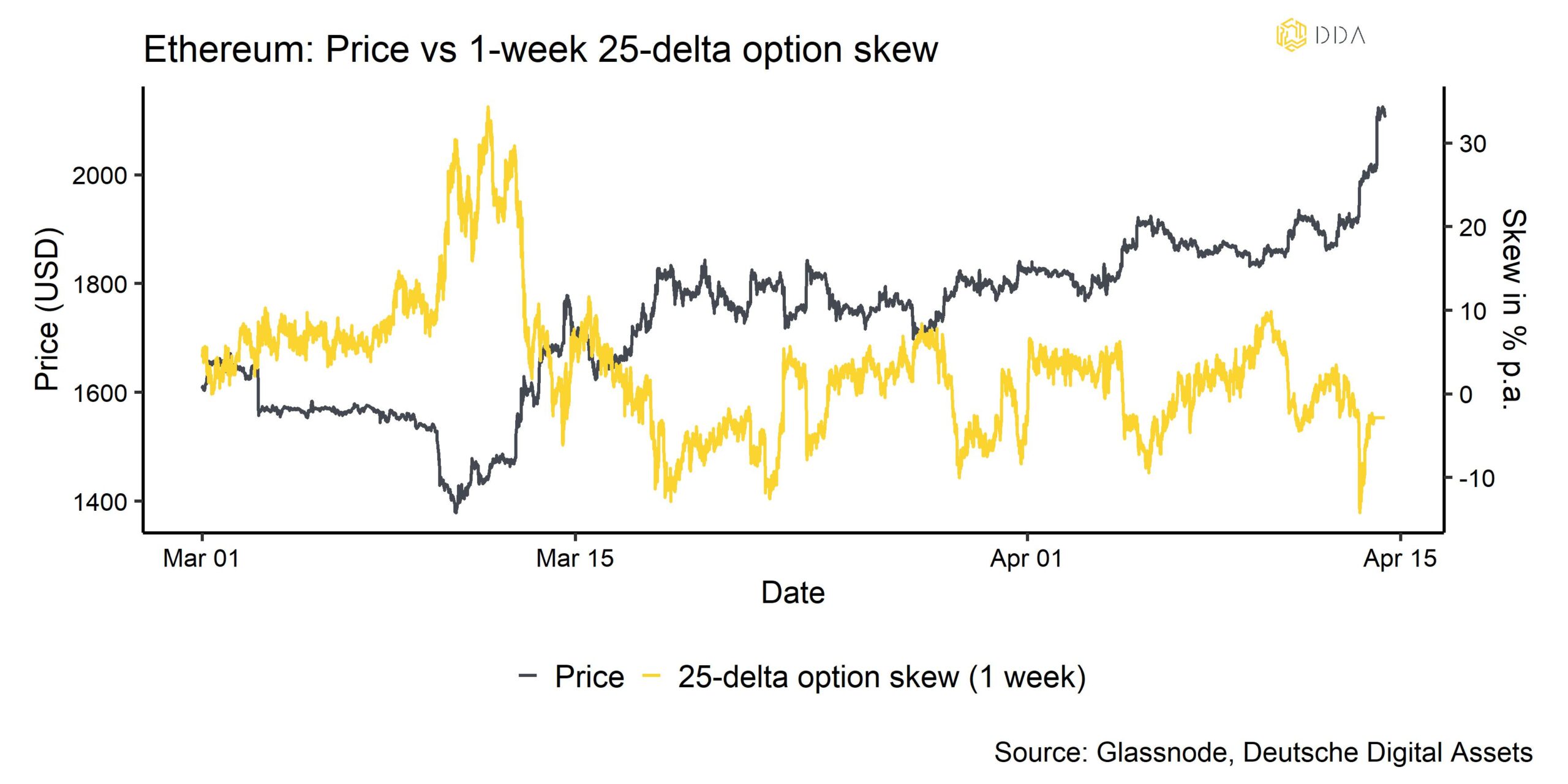

The decrease in risk aversion was particularly visible in the decrease in Ethereum 1-week option 25-delta skew, that measures the difference in put versus call implied volatilities for Ethereum options (see Chart-of-the-Week). Derivative traders were generally busy unwinding their downside hedges that were implemented before the upgrade.

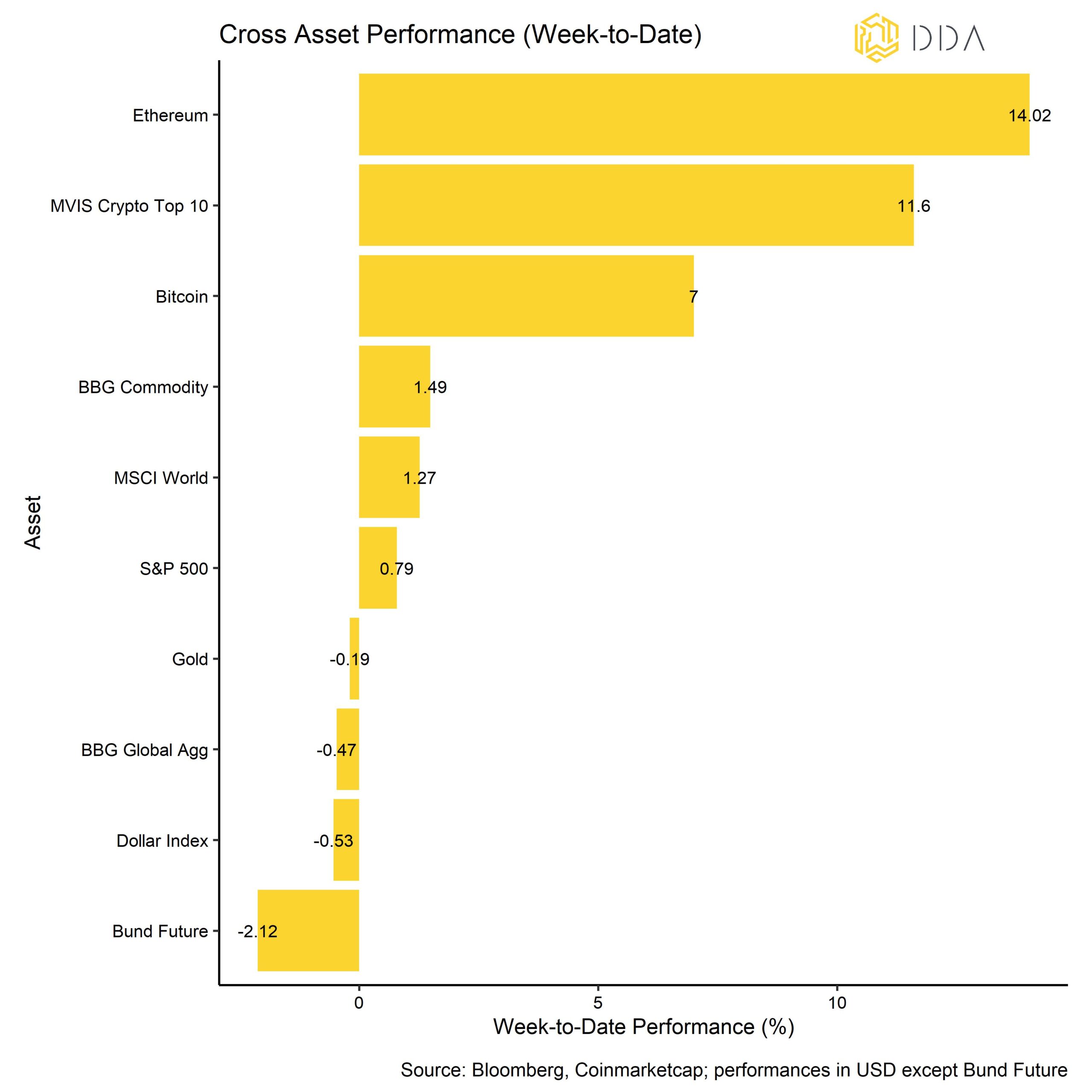

In comparison to traditional financial assets, cryptoassets have yet again outperformed by a very wide margin. Global bonds and the US Dollar were generally trading on the weak side last week while gold and global equities outperformed.

Among the major cryptoassets, Solana, Cardano, and Ethereum were the relative outperformers. There was generally an increase in risk appetite that resulted in some Altcoin outperformance, especially after the successful Ethereum upgrade.

Crypto Market Sentiment

Despite the continuing price increases, our in-house Crypto Sentiment Index has remained only slightly above neutral throughout the week which does not indicate any kind of exuberance in cryptoasset markets, yet. 12 out of 15 indicators are above their short-term trend.

Compared to last week, we saw major reversals in the global hedge fund beta to Bitcoin and the BTC Put-Call Volume Ratio.

The Crypto Fear & Greed Index has remained in “Greed” territory throughout the week.

Dispersion among cryptoassets has recently increased which means that cryptoassets are increasingly trading on systematic factors. At the same time, altcoin outperformance is still very low on a 1-week and 1-month basis. In general, altcoin outperformance goes hand in hand with a decrease in crypto dispersion, i.e. Bitcoin and altcoins are generally trading up systematically during “altseason” with altcoins outperforming Bitcoin. Altcoin outperformance is usually a sign of increased risk appetite and low altcoin outperformance is indicative of a rather cautious market sentiment. However, very low levels of altcoin outperformance should rather be considered a countercyclical buying opportunity.

Crypto Asset Flows

Last week saw a very significant net fund inflows into cryptoassets again.

In aggregate, we saw net fund inflows in the amount of +101.5 mn USD (week ending Friday) with the very large majority of inflows yet again flowing into Bitcoin funds (+111.5 mn USD). In contrast, Ethereum fund flows were rather flat last week (+1.8 mn USD) while both Altcoin funds ex Ethereum as well as Basket & Thematic Cryptoasset funds experienced net outflows (-3.6 mn USD and -8.2 mn USD, respectively).

Besides, the NAV discount of the biggest Bitcoin fund in the world – Grayscale Bitcoin Trust (GBTC) – has managed to narrow even further which implies some minor net inflows into this fund vehicle.

Probably one of the major changes compared to last week, was the fact that the beta of global Hedge Funds to Bitcoin over the last 20 trading days reversed into positive territory, implying that global hedge funds have changed their position and are now net long Bitcoin/cryptoassets.

Bitcoin prices traded on Coinbase vis-à-vis those traded on Binance (Coinbase-Binance premium) were mostly positive throughout the week, which is indicative of increased buying interest from institutional investors vis-à-vis retail investors.

On-Chain Activity

This week, much attention was on the Ethereum blockchain due to the Shapella upgrade that took place on Wednesday night last week. We have recently published a short “Crypto Espresso” report on the Ethereum Shapella upgrade. So, make sure to check it out if you have not done so already.

Before the upgrade, there was general uncertainty regarding the amount of ETH withdrawals and selling pressure after the unlock. A short-term spike in voluntary exists from the validator pool had created some minor uncertainty heading into the upgrade but the fact that both the amount of staked ETH kept increasing and the number of active validators decreased only slightly after the successful upgrade led to a broad decline in risk aversion. There was also a pick-up in new value staked and new validators after the upgrade which is also positive.

There were also no major ETH exchange inflows visible after the upgrade that would have indicated increasing selling pressure from staked ETH that had been unlocked.

According to beaconchain.in, around 468k withdrawals requests have already been processed with a total amount of around 1.023 mn ETH. However, according to on-chain data firm Nansen, there are still around 850k ETH of full withdrawals (i.e., principal withdrawals) waiting in the withdrawal queue. The Ethereum protocol limits the number of withdrawals to currently 115200 validator withdrawals per day. Should the withdrawal queue keep increasing in the coming days, this could exert some downward pressure on the price. However, withdrawals have generally slowed down in recent days.

Concerning Bitcoin, we saw a new year-to-date high in the number of active addresses on the Bitcoin blockchain last week which implies network activity is still supporting the positive price developments. However, there was some large exchange inflow from a whale address last Wednesday that amounted to 11236 BTC within a 10-minute interval. At the same time, a whale address was a recipient of a 23500 BTC (~710 million USD) transaction also on Wednesday which was the 4th largest recorded transfer of the year 2023. This could imply that a large institution or UHNWI investor has increased its exposure to Bitcoin.

Cryptoasset Derivatives

The recent price increase by Ethereum was certainly supported by derivatives markets. On the one hand, the recent drop in Ethereum 1-week option 25-delta skew implies that derivative traders were generally busy unwinding their downside hedges that were implemented before the upgrade (see Chart-of-the-Week).

Just before the upgrade, ETH options expiring right after the upgrade on the 13/4 and 14/4 were trading at significantly higher implied volatility premia than those right before the upgrade on 12/4. The so-called “volatility smile” was also largely skewed towards put options relative to call options for those options expiring after the upgrade. Thus, all in all, there was a significant amount of pre-upgrade hedging activity visible. This seems to have been wound down.

On the other hand, the increase in short liquidations on Ethereum futures contract implies that some traders were betting against a successful upgrade which now have been wrong footed and forced into liquidating their positions. This has certainly helped ETH advance to new highs as these traders are forced to buy back the underlying to neutralize their position. However, these short liquidations were still relatively small compared to the amount we have seen in early January or mid-March 2023.

Bitcoin futures saw also some minor short liquidations that helped advance the coin past 30k USD. Perpetual funding rates remained positive throughout the week indicating a general bias towards long perpetual contracts for Bitcoin. All in all, our in-house futures & perpetual positioning proxy for BTC still remains fairly subdued which implies that there is still significant potential for derivatives traders to increase their exposure to Bitcoin.

BTC implied volatilities are still fairly low as realized volatilities have continued to trend lower over while put-call open interest ratios have mostly moved sideways over the past week.

Bottom Line

The successful Ethereum Shapella upgrade as well as disappointing US macro data have led to just another upleg in cryptoasset prices.

Despite the recent price increases, our in-house Crypto Sentiment Index still remains neutral which signals no short-term exuberance so far.

Derivatives developments both for Bitcoin and Ethereum appear to be at the forefront of the recent price move once again as traders were generally busy unwinding their hedges after the upgrade.

About Deutsche Digital Assets

Deutsche Digital Assets is the trusted one-stop-shop for investors seeking exposure to crypto assets. We offer a menu of crypto investment products and solutions, ranging from passive to actively managed exposure, as well as financial product white-labeling services for asset managers.

We deliver excellence through familiar, trusted investment vehicles, providing investors the quality assurances they deserve from a world-class asset manager as we champion our mission of driving crypto asset adoption. DDA removes the technical risks of crypto investing by offering investors trusted and familiar means to invest in crypto at industry-leading low costs.

Legal Disclaimer

The material and information contained in this article is for informational purposes only. Deutsche Digital Assets, its affiliates, and subsidiaries are not soliciting any action based upon such material. This article is neither investment advice nor a recommendation or solicitation to buy any securities. Performance is unpredictable. Past performance is hence not an indication of any future performance. You agree to do your own research and due diligence before making any investment decision with respect to securities or investment opportunities discussed herein. Our articles and reports include forward-looking statements, estimates, projections, and opinions. These may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond Deutsche Digital Assets GmbH’s control. We believe all information contained herein is accurate, reliable and has been obtained from public sources. However, such information is presented “as is” without warranty of any kind.