A Closer Look at Cryptoasset Performance: Bitcoin Buying Interest, Central Bank Decisions and BNB Rumors

DDA Crypto Market Pulse, June 19, 2023

by André Dragosch, Head of Research

Key Takeaways

- Last week, cryptoasset performances were somewhat mixed due to the recent monetary policy decisions by major central banks, and due to some negative rumours associated with Binance’s BNB token

- Our in-house Crypto Sentiment Index has increased throughout last week and is in positive territory again

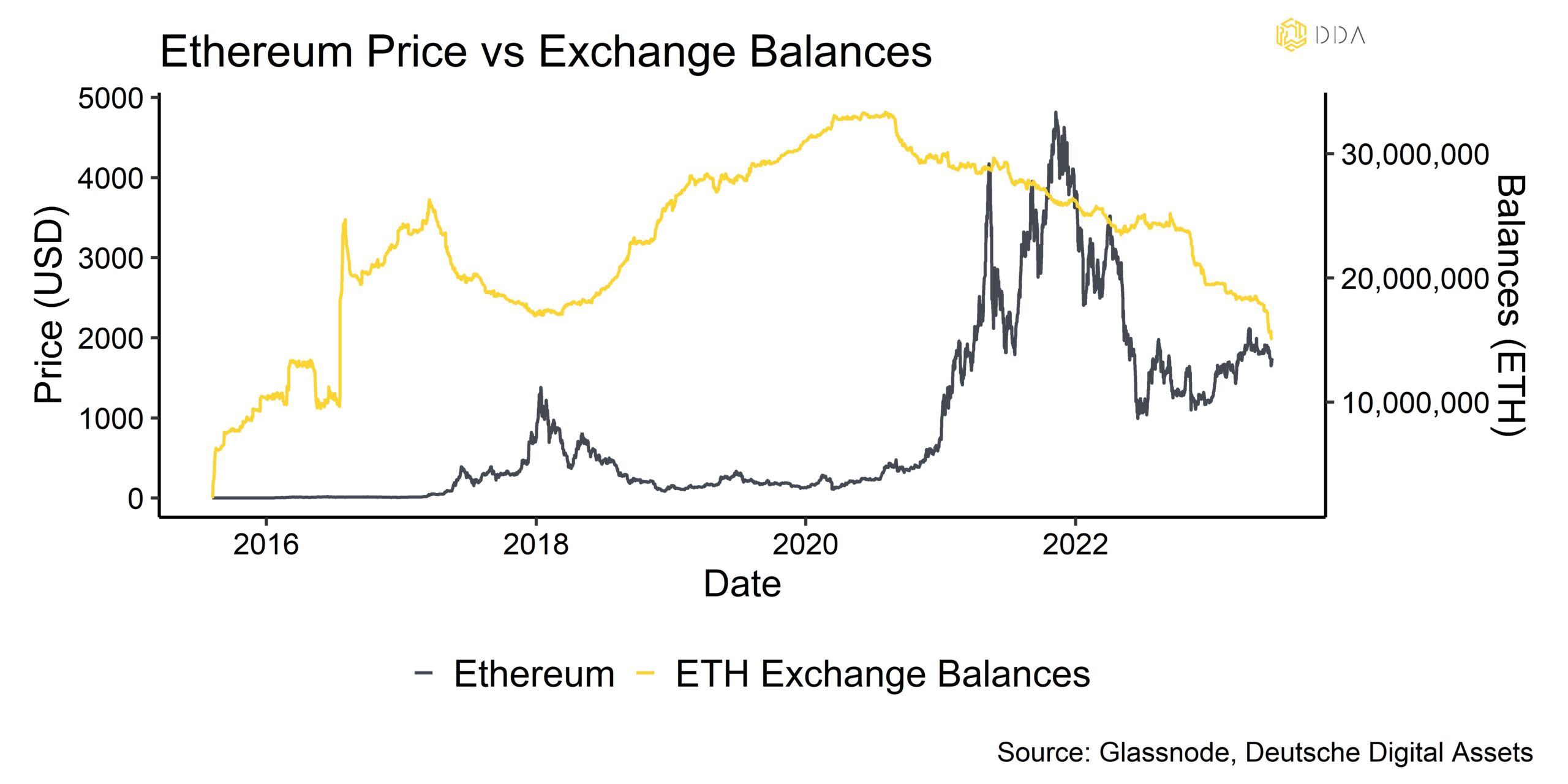

- Under the surface buying interest is still ongoing with continuing net exchange outflows for Bitcoin by large wallets and with exchange balances of Ethereum reaching a fresh 7-year low last week

Chart of the week

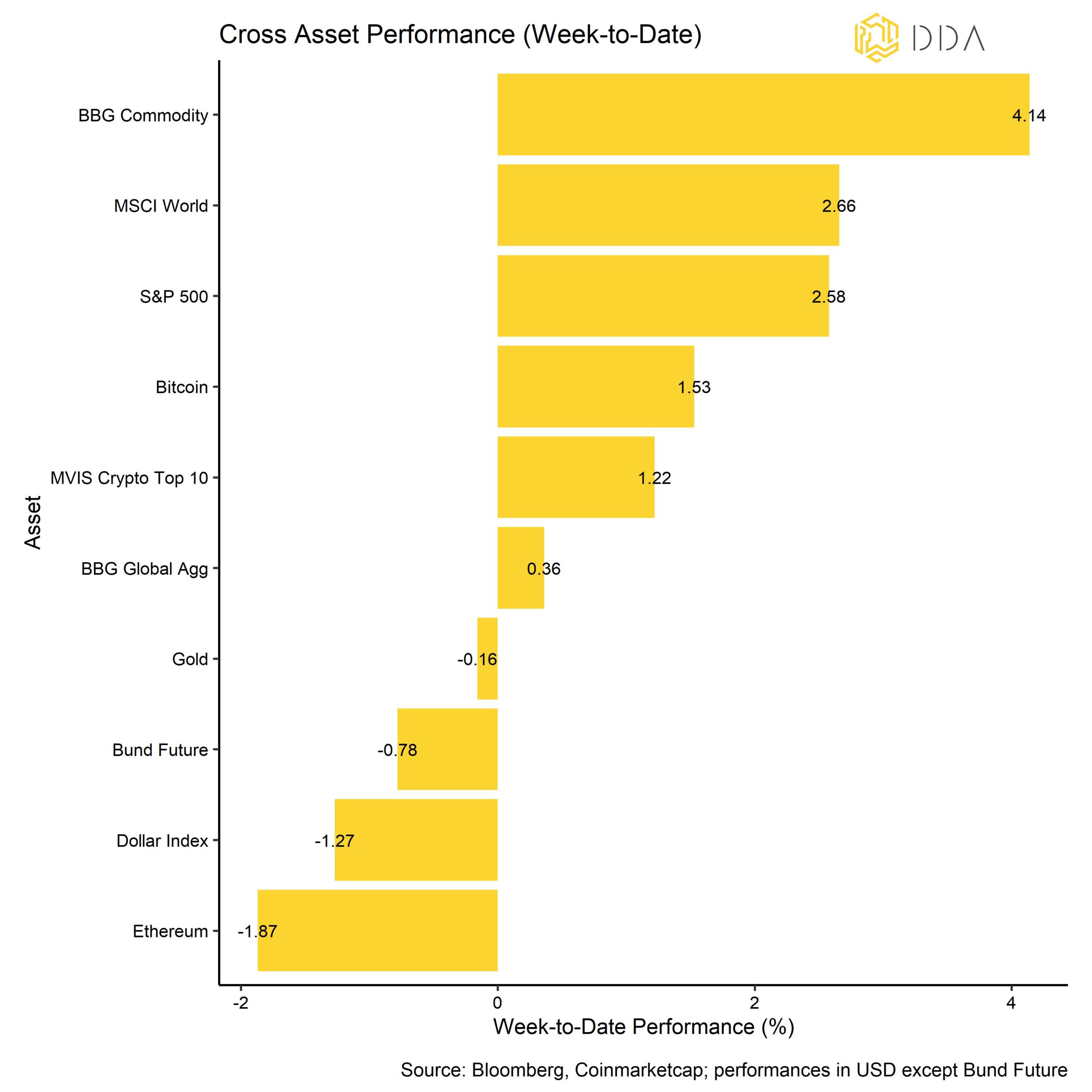

Cryptoasset Performance

Last week, cryptoasset performances were somewhat mixed due to the recent monetary policy decisions by major central banks, and due to some negative rumours associated with Binance’s BNB token.

More specifically, the Fed has delivered no hike in its June meeting but has telegraphed 50 BP in additional hikes until year-end in its Summary of Economic Projections (aka “dot plot”). Meanwhile, the ECB has also increased its deposit rate by 25 basis points to 3.5%. The good news is that the Fed has paused hiking for the first time in this hiking cycle that commenced in March 2022. Nonetheless, this had put some pressure on cryptoassets prices initially but prices have already reversed to the upside again.

A piece of news that supported overall market sentiment was the fact that Blackrock’s iShares has officially filed for a Bitcoin trust in the US. But unlike Grayscale’s Bitcoin Trust (GBTC), shares are expected to be redeemable as well which is why this is considered to be more akin to an “ETF”. However, the fact that Blackrock has filed for a trust increases the probability of approval significantly. In the US, authorities have already approved various Bitcoin futures ETFs but have so far refrained from approving spot, ie “phyiscally-backed”, Bitcoin ETFs. Therefore, an approval of this fund vehicle would be the first of its kind opening investment opportunities for institutional investors in the US.

Meanwhile, under the surface buying interest is still ongoing with continuing net exchange outflows for Bitcoin by large wallets and with exchange balances of Ethereum reaching a fresh 7-year low last week (Chart-of-the-Week).

All in all, the top 10 cryptoassets have performed positively but underperformed other major asset classes last week. Meanwhile, global equities continued to move up. Commodities were the best asset class again as the Dollar depreciated last week. Gold and bonds underperformed.

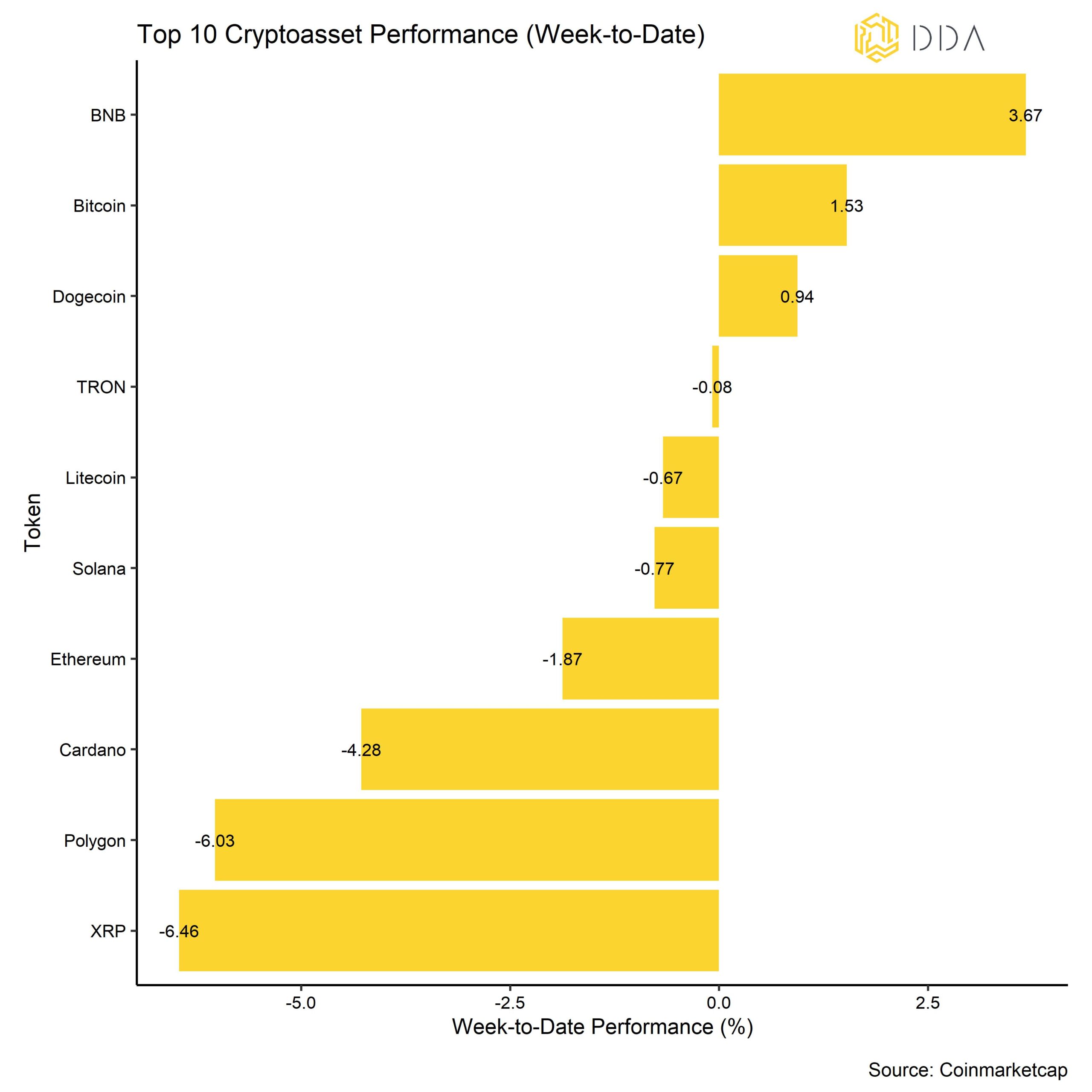

Among the top 10 cryptoassets, BNB, Bitcoin, and Dogecoin were the relative outperformers. Binance’s BNB token outperformed despite some negative rumours of market manipulation by its parent exchange Binance.

In general, altcoins were able to outperform Bitcoin again albeit from very low levels. Based on our set of tracked altcoins, only 25% of altcoins were able to outperform Bitcoin on a weekly basis.

Crypto Market Sentiment

Our in-house Crypto Sentiment Index has reversed significantly compared last week and is in positive territory again. 9 out of 15 indicators are still above their short-term trend.

Compared to last week, we saw major reversals to the upside in the Bitcoin option 25-delta skew and put-call volume ratios.

The Crypto Fear & Greed Index remains in “Neutral” territory as of this morning after having shortly slumped into “Fear” territory last week.

Performance dispersion among cryptoassets was recently unchanged compared to last week where performance dispersion had significantly decreased due to the SEC charges.

In general, high performance dispersion among cryptoassets implies that correlations among cryptoassets have decreased which means that cryptoassets are trading more on coin-specific factors.

At the same time, altcoin outperformance has increased slightly last week albeit from very low levels and is now at only 25% of altcoins outperforming Bitcoin on a weekly basis.

In general, altcoin outperformance goes hand in hand with an increase in crypto dispersion, i.e. Bitcoin and altcoins are generally trading up during “altseason” with altcoins outperforming Bitcoin. Broader altcoin outperformance is usually a sign of increasing risk appetite and broader altcoin underperformance a sign of increasing risk aversion.

Crypto Asset Flows

On a positive note, last week saw the first week of net fund flows into cryptoassets after 8 consecutive weeks of net fund outflows.

In aggregate, we saw slight net fund inflows in the amount of +0.9 mn USD (week ending Friday).

However, under the surface, there were significant divergences in fund flows.

While Bitcoin funds and Ethereum funds experienced net outflows (-0.3 mn USD and -6.0 mn USD, respectively) altcoin-based funds as well basket & thematic crypto funds both experienced net fund inflows last week (+1.3 mn USD and +5.9 mn USD, respectively).

Besides, the NAV discount of the biggest Bitcoin fund in the world – Grayscale Bitcoin Trust (GBTC) – has narrowed significantly which also implies some net inflows out of this fund vehicle.

Meanwhile, the beta of global Hedge Funds to Bitcoin over the last 20 trading days still remained flat, implying that global hedge funds have only a very minor positive net exposure to cryptoassets. However, the beta is still too small to consider it statistically significant. Global hedge funds still appear to be neutrally positioned with respect to cryptoassets at the moment.

On-Chain Activity

Bitcoin exchange transfers continued to pick up last week putting pressure on prices.

However, this was mostly due to transfers to exchanges by short-term holders (“weak hands”) who realized losses. In fact, exchange transfers in loss by these short-term holders were the highest since the SVB collapse in March last week.

Furthermore, Bitcoin miners’ transfers to exchanges increased even further and have surpassed 3000 BTC per day last week. As mentioned in the last CMP report, Bitcoin miners have recently come under financial pressure due to the relentless increase in hash rate.

On a positive note, long-term holders (“strong hands”) do not appear to be taking neither significant amounts of losses nor profits at the moment which is a positive sign.

In general, BTC continued to flow out of exchanges on a net basis. In particular, we saw significant outflows by larger wallet sizes containing 10 mn USD in BTC or more last week on Thursday. Meanwhile, Ethereum exchange inflows have abated significantly last week. Even more so, ETH continued to flow out of exchanges significantly last week which is a very positive sign. As a result, Ethereum exchange balances reached the lowest level since July 2016 (Chart-of-the-Week).

Cryptoasset Derivatives

Last week, we saw major reversals to the upside in the Bitcoin 1-month 25-delta option skew as well as the put-call volume ratio both of which imply a positive reversal in option market sentiment.

We also saw a significant increase in the Bitcoin 3-months basis rate which increased above 3% p.a. again. This also signals an improving price outlook by futures traders. The perpetual funding rate for Bitcoin also remained slightly positive throughout last week.

Both futures and perpetual open interest for Bitcoin gradually increased last week in BTC-terms.

Bottom Line

Last week, cryptoasset performances were somewhat mixed due to the recent monetary policy decisions by major central banks, and due to some negative rumours associated with Binance’s BNB token.

Our in-house Crypto Sentiment Index has increased throughout last week and is in positive territory again.

Under the surface buying interest is still ongoing with continuing net exchange outflows for Bitcoin by large wallets and with exchange balances of Ethereum reaching a fresh 7-year low last week.

About Deutsche Digital Assets

Deutsche Digital Assets is the trusted one-stop-shop for investors seeking exposure to crypto assets. We offer a menu of crypto investment products and solutions, ranging from passive to actively managed exposure, as well as financial product white-labeling services for asset managers.

We deliver excellence through familiar, trusted investment vehicles, providing investors the quality assurances they deserve from a world-class asset manager as we champion our mission of driving crypto asset adoption. DDA removes the technical risks of crypto investing by offering investors trusted and familiar means to invest in crypto at industry-leading low costs.

Legal Disclaimer

The material and information contained in this article is for informational purposes only. Deutsche Digital Assets, its affiliates, and subsidiaries are not soliciting any action based upon such material. This article is neither investment advice nor a recommendation or solicitation to buy any securities. Performance is unpredictable. Past performance is hence not an indication of any future performance. You agree to do your own research and due diligence before making any investment decision with respect to securities or investment opportunities discussed herein. Our articles and reports include forward-looking statements, estimates, projections, and opinions. These may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond Deutsche Digital Assets GmbH’s control. We believe all information contained herein is accurate, reliable and has been obtained from public sources. However, such information is presented “as is” without warranty of any kind.