Download the Full Report in PDF

by André Dragosch, Head of Research

Key Takeaways

- Cryptoassets were again the best asset class last week, outperforming global equities, bonds and commodities

- Our in-house Crypto Sentiment Index has improved further as underlying sentiment was mainly supported by the positive statements of Fed Chairman Powell

- In general, exchange inflows have leveled off as well, implying overall less selling pressure, which is also true for Bitcoin miner’s transfers to exchanges

Chart of the Week

Performance

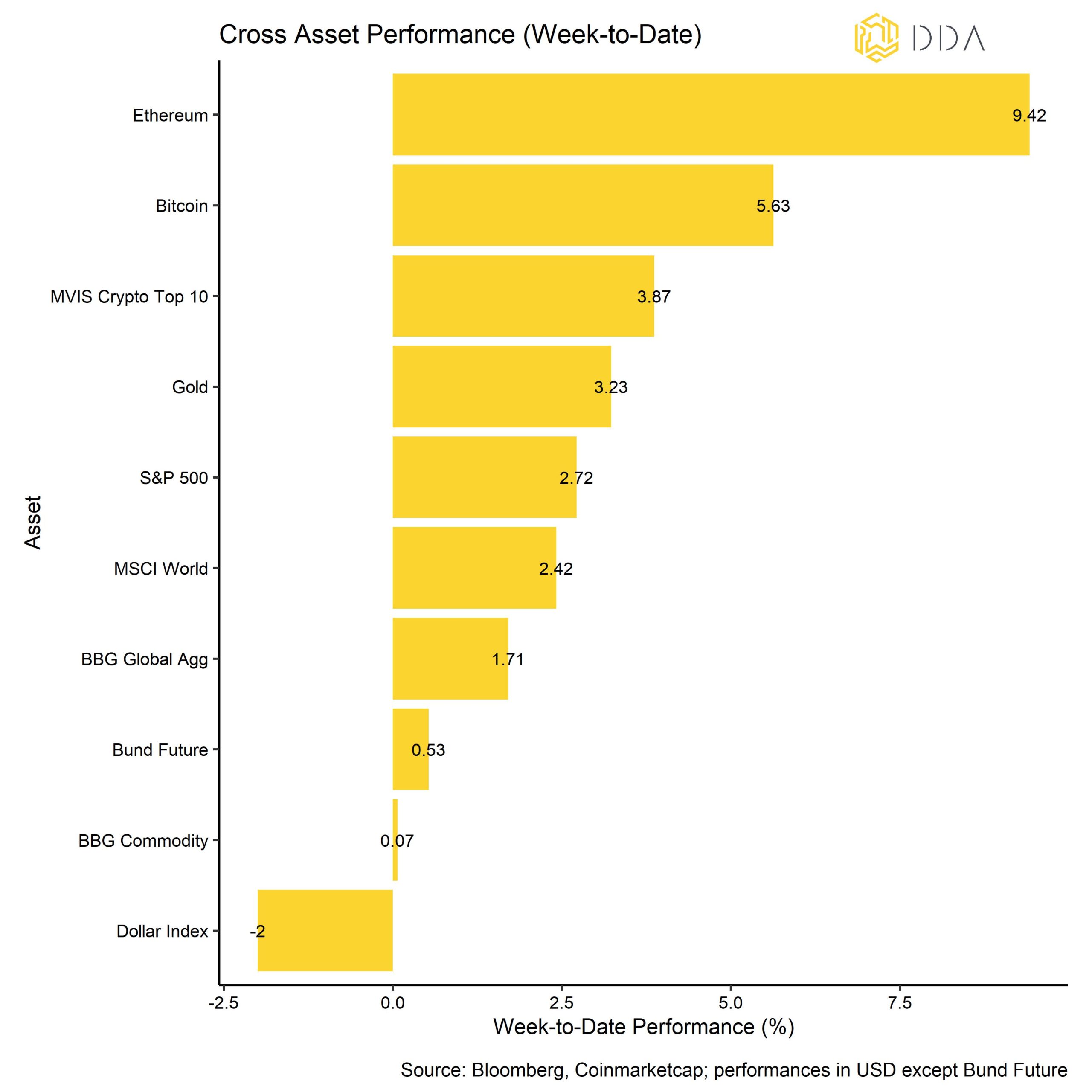

Last week, cryptoasset prices managed to outperform again, being supported by the news that “it makes sense to moderate the pace of our rate hikes” for the Federal Reserve as soon as December. This statement was made by Fed Chairman Powell last week.

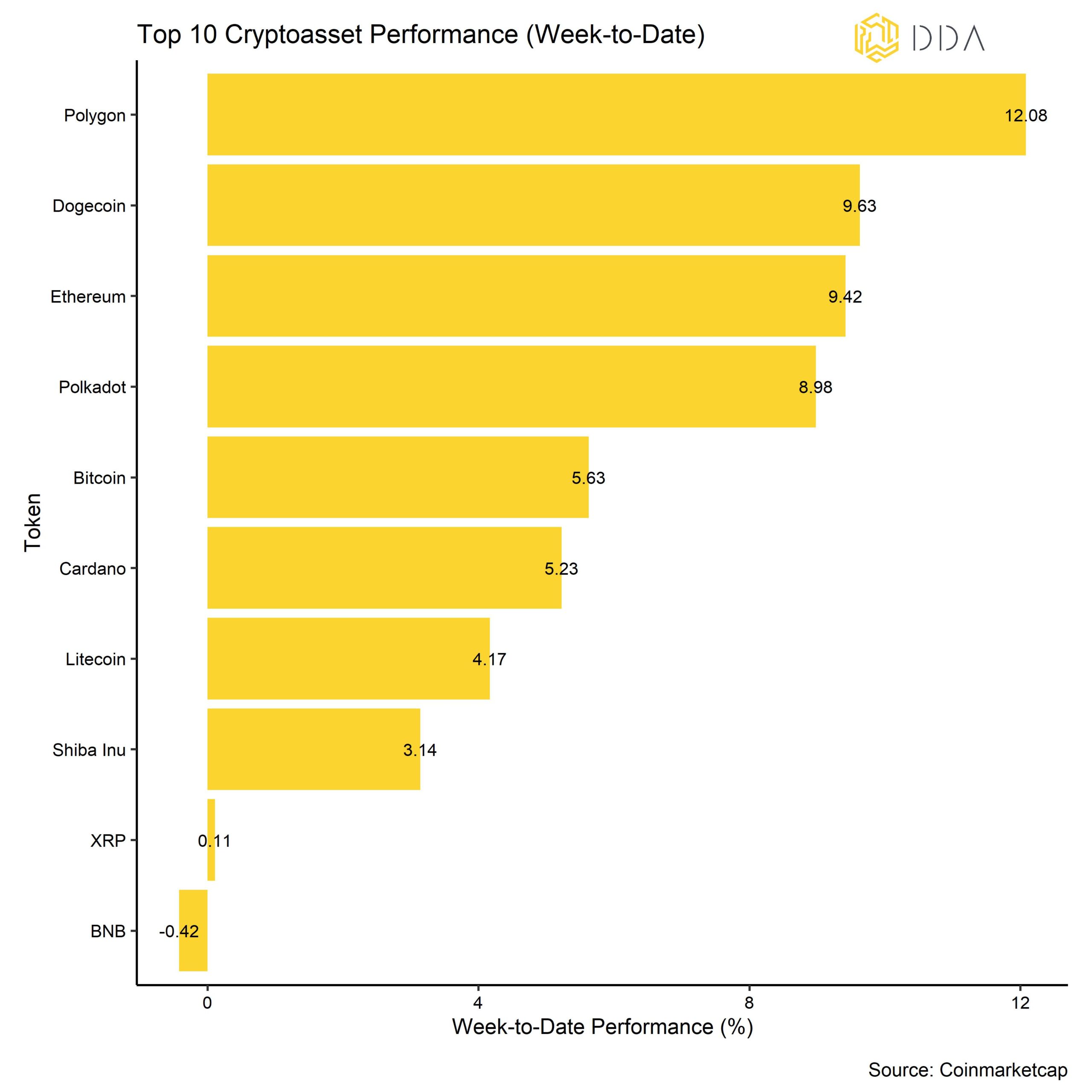

Accordingly, cryptoasset prices and other risky assets have mostly performed positively. Among the major cryptoassets, Polygon, Dogecoin and Ethereum were the relative outperformers. Cryptoassets were once again the best asset class last week, outperforming global equities, commodities and bonds. The Dollar weakened last week again.

Sentiment

Our in-house Crypto Sentiment Index has improved further compared to last week and has shortly entered into positive territory. That means that the majority of our indicators were above their short-term trend. The major contributors were the increase in hedge fund beta to BTC as well as the reversals in BTC options’ implied volatilities and funding rates which are usually indicative of an increase in risk appetite within cryptoassets.

Dispersion among cryptoassets on a rolling basis was still very low, implying that the cryptomarket was rather trading on systematic factors than on coin-specific factors. At the same time, altcoins mostly managed to outperform Bitcoin which is usually a sign of increasing risk appetite.

The Crypto Fear & Greed Index improved as well but is still in “Fear” territory.

Flows

Fund flows continued to be weak during the last week and we saw net outflows out of global crypto ETPs in the amount of -4.0 mn USD. However, Bitcoin-based products fared rather well and experienced inflows of +13.7 mn USD net over the week while all other crypto ETP products experienced net outflows.

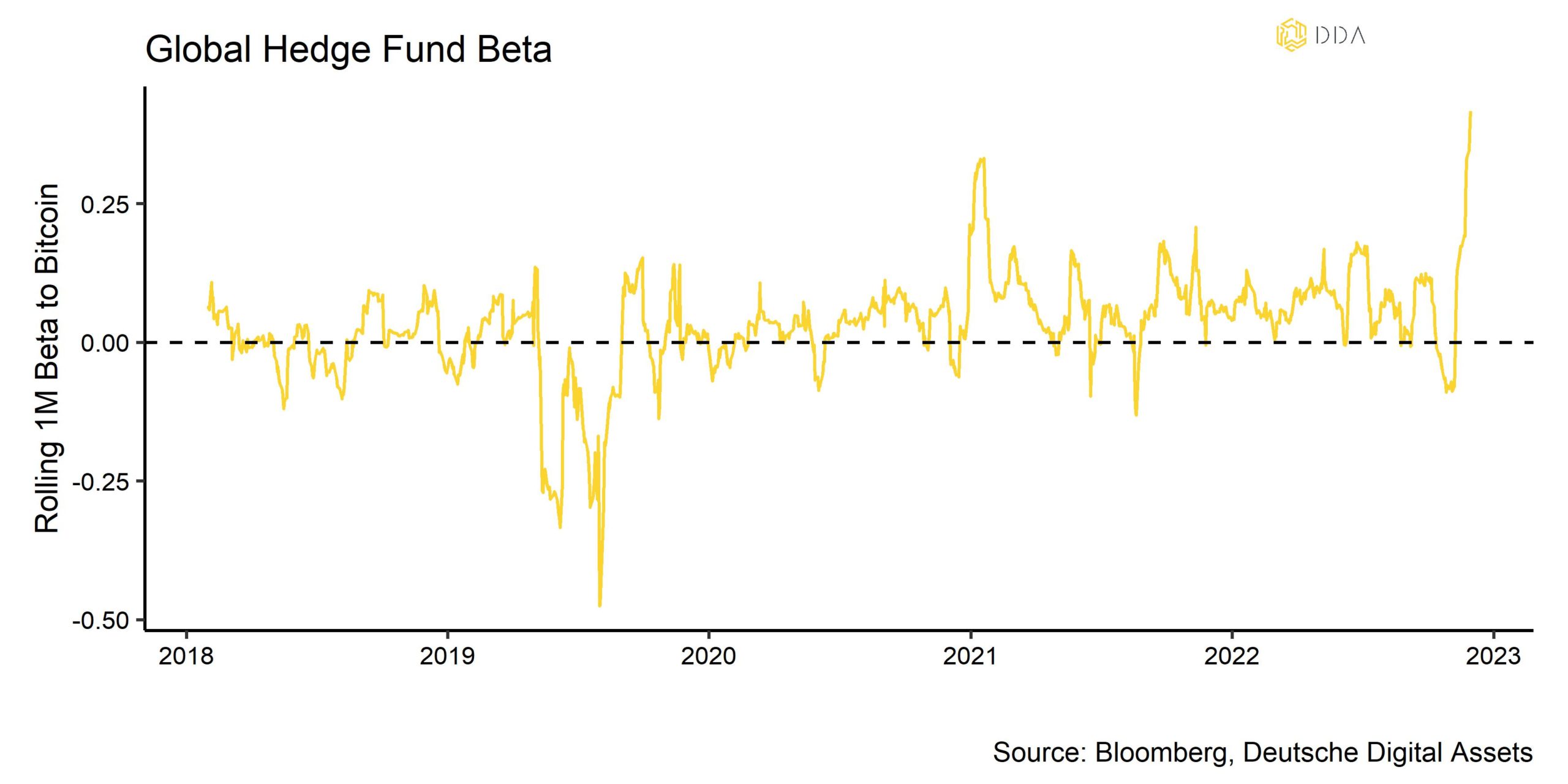

On a positive note, the Beta of global Hedge Funds to Bitcoin over the last 20 trading days continued to rise, implying that hedge funds might have further increased their exposure to cryptoassets during the month. The beta of global hedge funds to Bitcoin increased to the highest reading since 2018 which implies a significant increase in hedge funds’ exposure to cryptoassets during the last 20 trading days.

Another highlight is that the Coinbase-Binance premium continued to be positive throughout the week which is indicative of relative buying interest from institutional investors vis-à-vis retail investors.

On-Chain

In general, exchange inflows have leveled off as well, implying overall less selling pressure.

There were no significant exchange flows neither from nor to exchanges during last week.

It seems that we are slowly entering the rather calm Christmas season as Bitcoin transactions volumes have declined to a 2-year low.

BTC miners’ transfers to exchanges declined as well compared to last week, when we noticed the highest transfers year-to-date, implying that selling pressure has somewhat receded.

We have highlighted the increased risk of “miner capitulation” in our latest issue of the “Crypto Market Intelligence” report as well. The decrease in miner exchange inflows is a positive development in this regard.

Another highlight is that short-term hodlers with a holding period of less than 155 days, managed to realize profits again after weeks of realizing harsh losses which usually improves overall market sentiment as well.

However, OTC desk holdings of Bitcoin are still very low and don’t imply significant buying interest by institutional investors, yet.

Derivatives

In general, we saw some significant moderation in risk aversion within the Bitcoin derivatives markets. This is evident in the continuing decrease in Bitcoin Implied volatilities and a normalization in the skew. The sharp reversal in perpetual funding rates is also indicative of a gradual unwind of downside hedges and a reduction in risk aversion among derivatives traders.

Bottom Line

Cryptoassets were again the best asset class last week, outperforming global equities, bonds and commodities.

Our in-house Crypto Sentiment Index has improved further as underlying sentiment was mainly supported by Fed Chairman Powell’s statement to moderate the pace of rate hikes as soon as December. Crypto ETP fund flows slightly negative except for Bitcoin ETPs while global hedge funds’ beta to Bitcoin increased even further. On-chain indicators imply that overall selling pressure has receded as exchange inflows have declined compared to last week. Miner’s transfers to exchanges have also declined which is a positive development in light of a potential “miner capitulation”.

Besides, we saw another significant moderation in risk aversion within the Bitcoin derivatives markets.

Download the full report with appendix here.

About Deutsche Digital Assets

Deutsche Digital Assets is the trusted one-stop-shop for investors seeking exposure to crypto assets. We offer a menu of crypto investment products and solutions, ranging from passive to actively managed exposure, as well as financial product white-labeling services for asset managers.

We deliver excellence through familiar, trusted investment vehicles, providing investors the quality assurances they deserve from a world-class asset manager as we champion our mission of driving crypto asset adoption. DDA removes the technical risks of crypto investing by offering investors trusted and familiar means to invest in crypto at industry-leading low costs.

Recent News and Articles

- Institutional Crypto Adoption: Why & How Institutions Are Going Crypto

- Crypto Portfolio Composition: How Different Portfolios Have Performed During the Recent Bull and Bear Markets

- How to Invest in Ethereum (ETH): A Guide for Professional Investors

- The Case for Actively Managed Investment Strategies in the Crypto Markets

- How to Invest in NFTs: A Guide for Professional Investors

- Why Bitcoin’s Volatility Shouldn’t Scare You

- How accurate is the Bitcoin Stock-to_Flow Model?

Deutsche Digital Assets in Press

- ETF stream: White-label issuers in Europe quietly tripled in a week

- Das Investment: Kryptowährungen kommen 2022 im Mainstream an

- Private Banking Magazin, Bitcoin – das perfekte Beispiel für ein ESG-Investment?

- Institutional Money, Krypto-Manager steigt bei Family Office ein

Legal Disclaimer

The material and information contained in this article is for informational purposes only. Deutsche Digital Assets, its affiliates, and subsidiaries are not soliciting any action based upon such material. This article is neither investment advice nor a recommendation or solicitation to buy any securities. Performance is unpredictable. Past performance is hence not an indication of any future performance. You agree to do your own research and due diligence before making any investment decision with respect to securities or investment opportunities discussed herein. Our articles and reports include forward-looking statements, estimates, projections, and opinions. These may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond Deutsche Digital Assets GmbH’s control. We believe all information contained herein is accurate, reliable and has been obtained from public sources. However, such information is presented “as is” without warranty of any kind.