Cryptoassets: There is no second best? The advantages & disadvantages of portfolio diversification

by André Dragosch, Head of Research

Key Takeaways

- From a pure statistical point of view, most Altcoins are high beta and negative theta derivatives of Bitcoin (BTC). There are few Altcoins among the top 10 that have exhibited a systematic outperformance (alpha) that is not explained by relatively higher market risk (beta)

- Exceptions are Binance Coin (BNB), Solana (SOL), Polygon (MATIC), and TRON (TRX) that exhibit a positive theta relative to Bitcoin (BTC)

- Altcoins do have a place in a diversified portfolio of cryptoassets but Bitcoin (BTC) should be a core holding of the passive portfolio itself – this is amongst other things also reflected in the construction of our DDA Crypto Select 10 ETP (SLCT)

There is no second best?

Bitcoin maximalists, i.e. those who advocate investing in Bitcoin only, point to the fact that Bitcoin (BTC) has always been the most dominant asset by market capitalization since its inception in 2009. This implies that Bitcoin has consistently outperformed other cryptoassets over the past 14 years.

In fact, there are very few cryptoassets that have managed to outperform Bitcoin over the course of various market cycles: So far, only Ripple (XRP), Dogecoin (DOGE), and Ethereum (ETH) managed to outperform Bitcoin (BTC) over two market cycles, ie managed to make two new highs in relative terms (denominated in Bitcoin).

That being said, an important question for cryptoasset investors remains whether diversification into “Altcoins”, ie everything else than Bitcoin, still makes sense from a pure statistical and performance point of view?

In the following paragraphs, we will outline the respective advantages and disadvantages of diversification and how the optimal passive portfolio allocation for investors might look like.

The Alpha, Beta and Theta of Altcoins

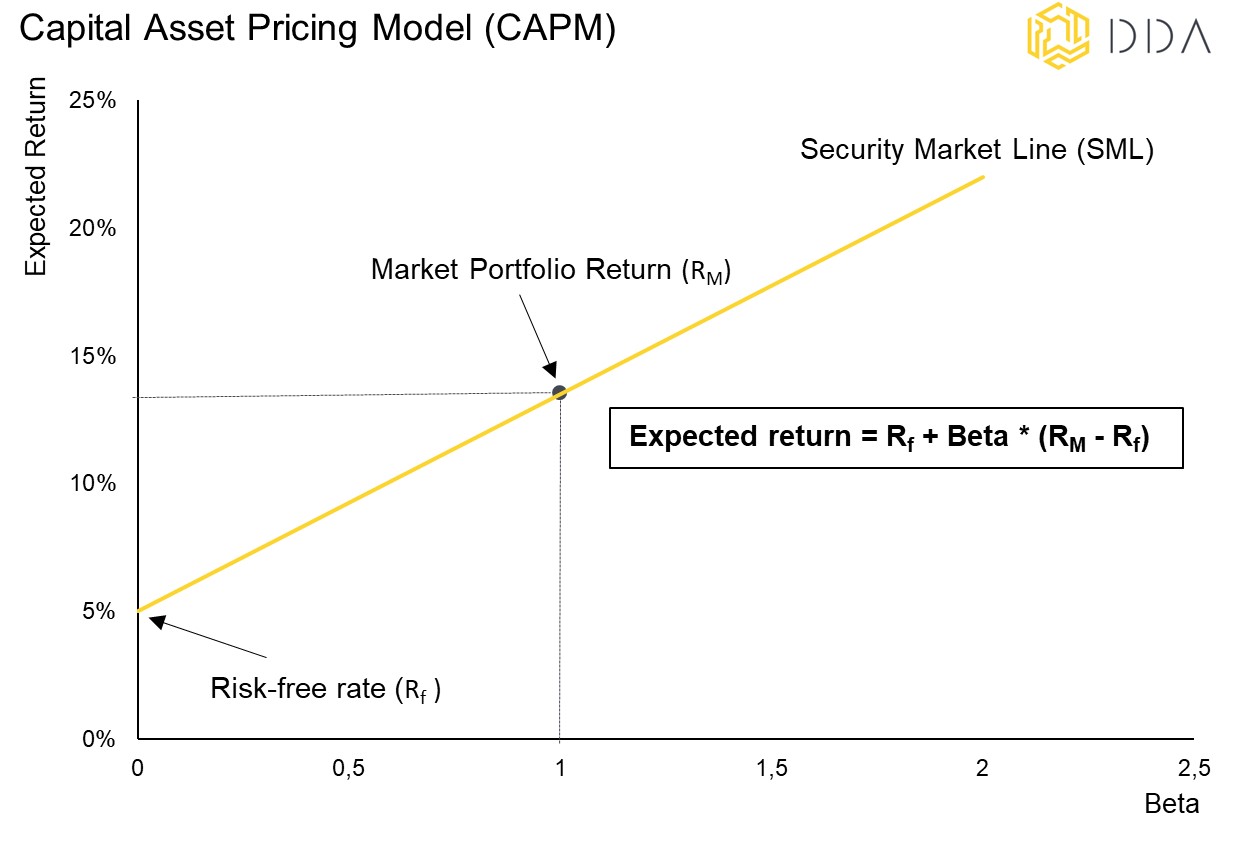

The traditional Capital Asset Pricing Model (CAPM) first proposed by Nobel laureate William Sharpe and others in the 1960s implies that there is no free lunch and there is a tight relationship between (non-diversifiable) risk and return:

Higher returns are usually associated with higher market risks (beta > 1) and vice versa.

William Sharpe and others came up with the idea that excess returns could be due to excess risk being taken by the investor compared to a market benchmark asset that represents a non-diversifiable risk.

This is widely known as “beta” which describes the relative sensitivity of an asset relative to a benchmark asset that is representative for the asset class.

However, there are exceptions. Some individual assets might exhibit excess performances over benchmark returns that are not associated with relatively higher market risk (beta) which is widely known as “alpha”.

Professional investors have been on the look-out for systematic alpha ever since, that is a consistent outperformance of the benchmark asset that is not associated with relatively higher risks.

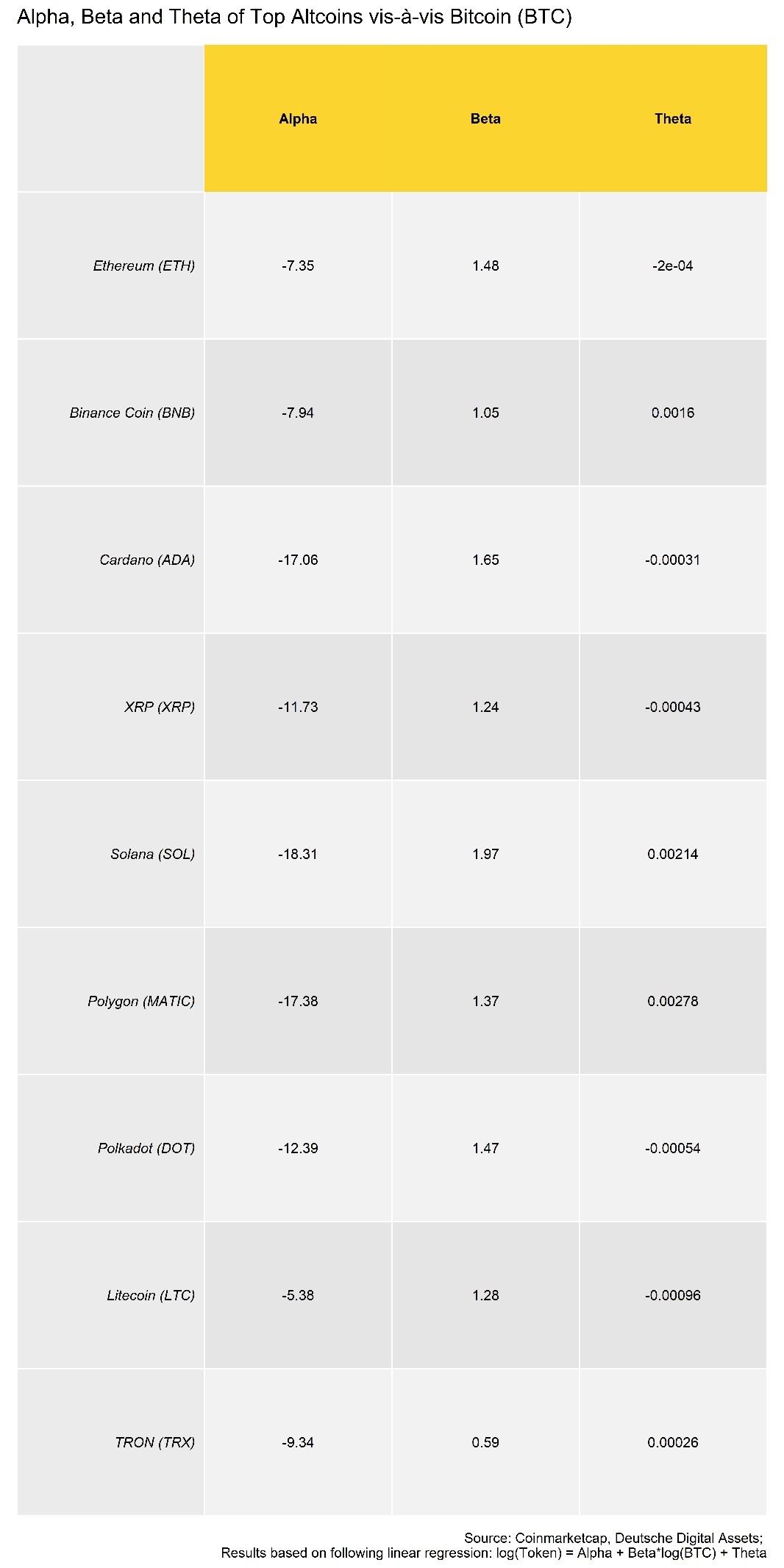

To shed more light on this issue, we have looked at the major large cap cryptoassets among the top 10 by market capitalization and looked at their respective Alpha, Beta and Theta with respect to Bitcoin.

We have estimated the following linear regression:

Log(Token) = Alpha + Beta * log(BTC) + Theta

With Alpha being the regression constant, Beta being the sensitivity of the Token relative to BTC and Theta being a time trend measured in days since the start of the sample period.

The regressions are based on Ordinary-Least-Squares (OLS) and were performed based on daily prices that utilize the longest available time series provided by Coinmarketcap. All the estimated coefficients are highly significant.

The following table presents the result of these regressions:

As can be seen in the abovementioned table, none of the altcoins exhibit an outperformance (positive alpha) of Bitcoin (BTC) in excess of their relatively higher volatility (beta > 1.0) to Bitcoin. The majority of altcoins also exhibit a historical beta that is greater than 1 with the exception of TRON (TRX). A beta coefficient greater than 1 implies that the token increases/decreases by the beta factor relative to Bitcoin. For instance if the token exhibits a beta of 1.5, an increase in Bitcoin by 1% was associated with an increase in the token by 1.5% in the past.

Moreover, the amount of outperformance (alpha) conditional on the relative volatility (beta) and time trend (theta) is always negative.

The only exceptions are Binance Coin (BNB), Solana (SOL), Polygon (MATIC), and TRON (TRX) that exhibit a positive theta relative to Bitcoin (BTC).

This means that apart from their higher risk, there is positive optionality in holding these tokens over a longer term from a pure statistical point of view.

For the other tokens, a negative theta and beta above 1.0 implies that these tokens outperform Bitcoin (BTC) in a bull market but that the prices decay structurally vis-à-vis Bitcoin over the longer term.

Thus, from a pure statistical point of view, there is negative optionality associated with holding these tokens in the long run.

Please note though that these historical results might change in the future.

Altcoins: A cold shower?

When it comes to strategic/passive portfolio construction, professional investors are mostly concerned about two aspects:

The degree of outperformance by non-core holdings (in our case altcoins versus Bitcoin) and the degree of diversification added by these non-core holdings (relative correlation versus Bitcoin).

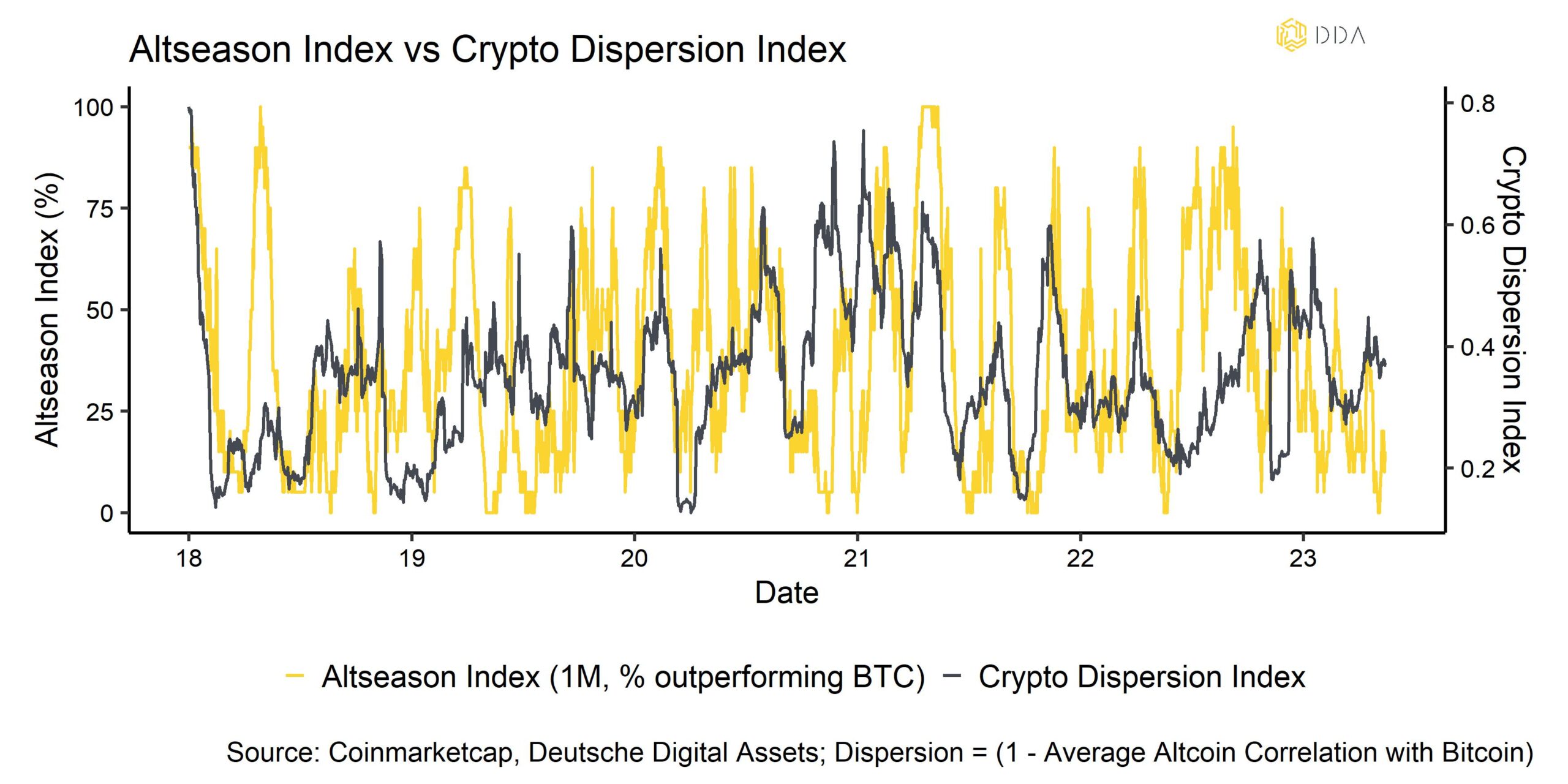

In general, altcoins tend to outperform Bitcoin (BTC) in bull markets when performance dispersion among them increases/correlations decrease and they start trading more on token-specific factors rather than systematic factors.

In contrast, there is usually a decrease in dispersion among altcoins during bear markets that is associated with an underperformance vis-à-vis Bitcoin (BTC) when altcoins mostly trade in the same direction as Bitcoin.

This is also depicted in the following chart that shows a positive relationship between the % of altcoins outperforming Bitcoin on 1-month basis (“Altseason Index”) and the average dispersion among altcoins (“Crypto Dispersion Index”):

- Usually there is high altcoin outperformance and high crypto dispersion during bull markets (i.e. rising BTC price) and vice versa.

In other words, there are also less benefits from diversification into altcoins during bear markets when dispersion among cryptoassets tends to decline (correlation tends to increase), and altcoin outperformance vis-à-vis Bitcoin is usually low.

But in bull markets, other altcoins might be able to outperform Bitcoin (BTC) due to their higher beta. Therefore, professional investors should treat most altcoins as a cold shower: move in during bull markets but move out during bear markets.

All in all, the results imply that some altcoins do have a place in a diversified portfolio of cryptoassets but that Bitcoin (BTC) should be a core holding of the passive portfolio itself.

Amongst other aspects, this rationale is also reflected in our DDA Crypto Select 10 ETP (ISIN: DE000A3G3ZD0, WKN: A3G3ZD, ticker: SLCT) that we have recently launched.. You can find more information here.

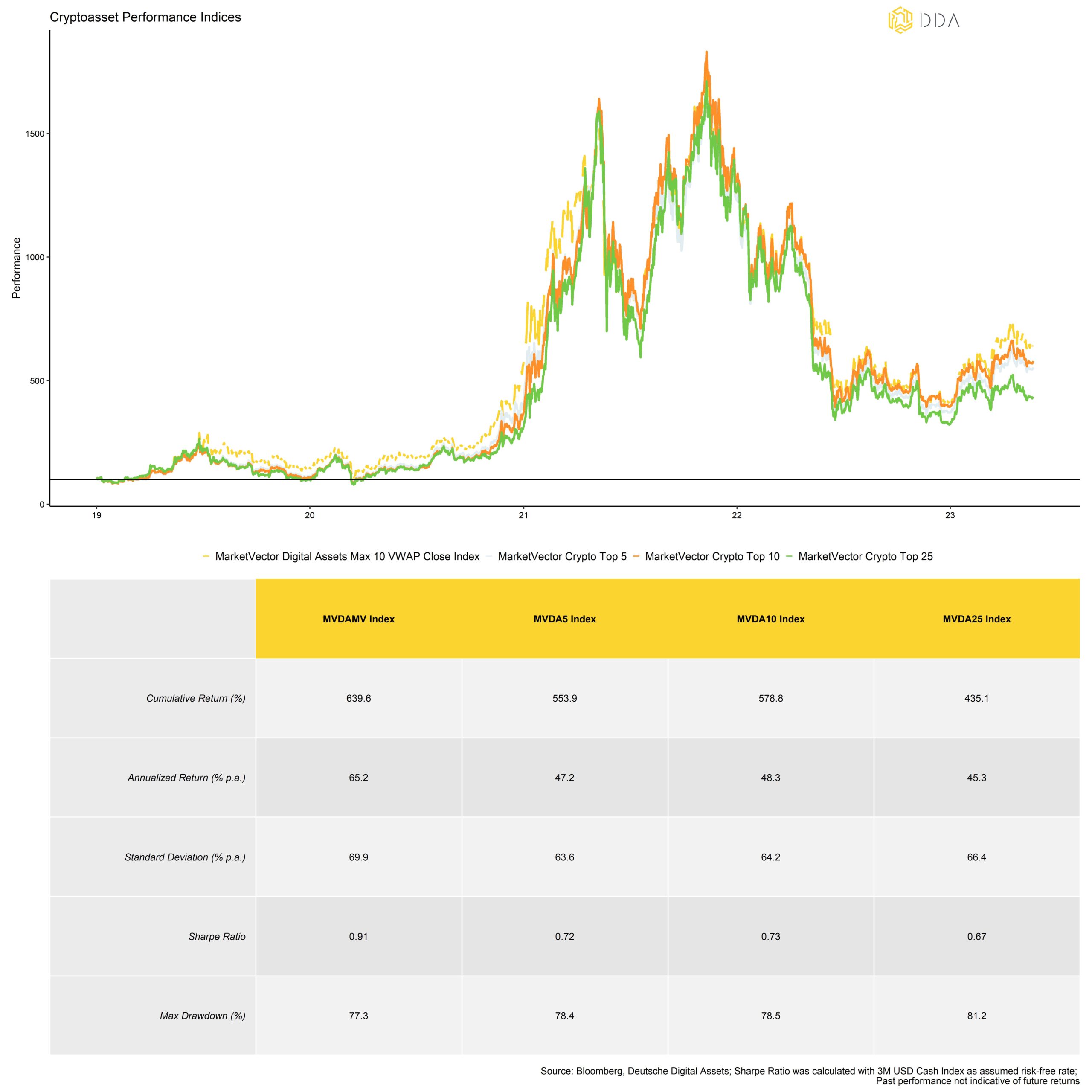

While other basket ETP concepts employ a capped weighting scheme that leads to a relatively low weighting of Bitcoin (BTC), SLCT – which follows the MarketVector Digital Assets Max 10 VWAP Close Index – employs an uncapped weighting scheme.. A decision that has been consciously made to to reap most of the statistical benefits for investorsA performance comparison of the ETP’s underlying index benchmark (MarketVector Digital Assets Max 10 VWAP Close Index, MVDAMV) reveals that it exhibits the highest (historical) cumulative return, highest risk-adjusted return (Sharpe Ratio) and the lowest maximum drawdown compared to other capped benchmarks that track the top large cap cryptoassets:

Bottom Line:

From a pure statistical point of view, most Altcoins are high beta and negative theta derivatives of Bitcoin (BTC). There are few Altcoins among the top 10 that have exhibited a systematic outperformance that is not explained by relatively higher market risk (beta).

Exceptions are Binance Coin (BNB), Solana (SOL), Polygon (MATIC), and TRON (TRX) that exhibit a positive theta relative to Bitcoin (BTC).

Altcoins do have a place in a diversified portfolio of cryptoassets but Bitcoin (BTC) should be a core holding of the passive portfolio itself – this is amongst other things also reflected in the construction of our DDA Crypto Select 10 ETP (SLCT).

Sign up for the DDA Newsletter here and receive our latest research reports, weekly market analysis and the latest insights on macro, industrial and crypto market trends from our top experts, delivered straight to your inbox.

Legal Disclaimer

The material and information contained in this article is for informational purposes only. Deutsche Digital Assets, its affiliates, and subsidiaries are not soliciting any action based upon such material. This article is neither investment advice nor a recommendation or solicitation to buy any securities. Performance is unpredictable. Past performance is hence not an indication of any future performance. You agree to do your own research and due diligence before making any investment decision with respect to securities or investment opportunities discussed herein. Our articles and reports include forward-looking statements, estimates, projections, and opinions. These may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond Deutsche Digital Assets GmbH’s control. We believe all information contained herein is accurate, reliable and has been obtained from public sources. However, such information is presented “as is” without warranty of any kind.