Whales on the Move: Examining Bitcoin’s Significant Exchange Inflows and US Bitcoin Spot ETF Effect

DDA Crypto Market Pulse, September 04, 2023

by André Dragosch, Head of Research

Key Takeaways

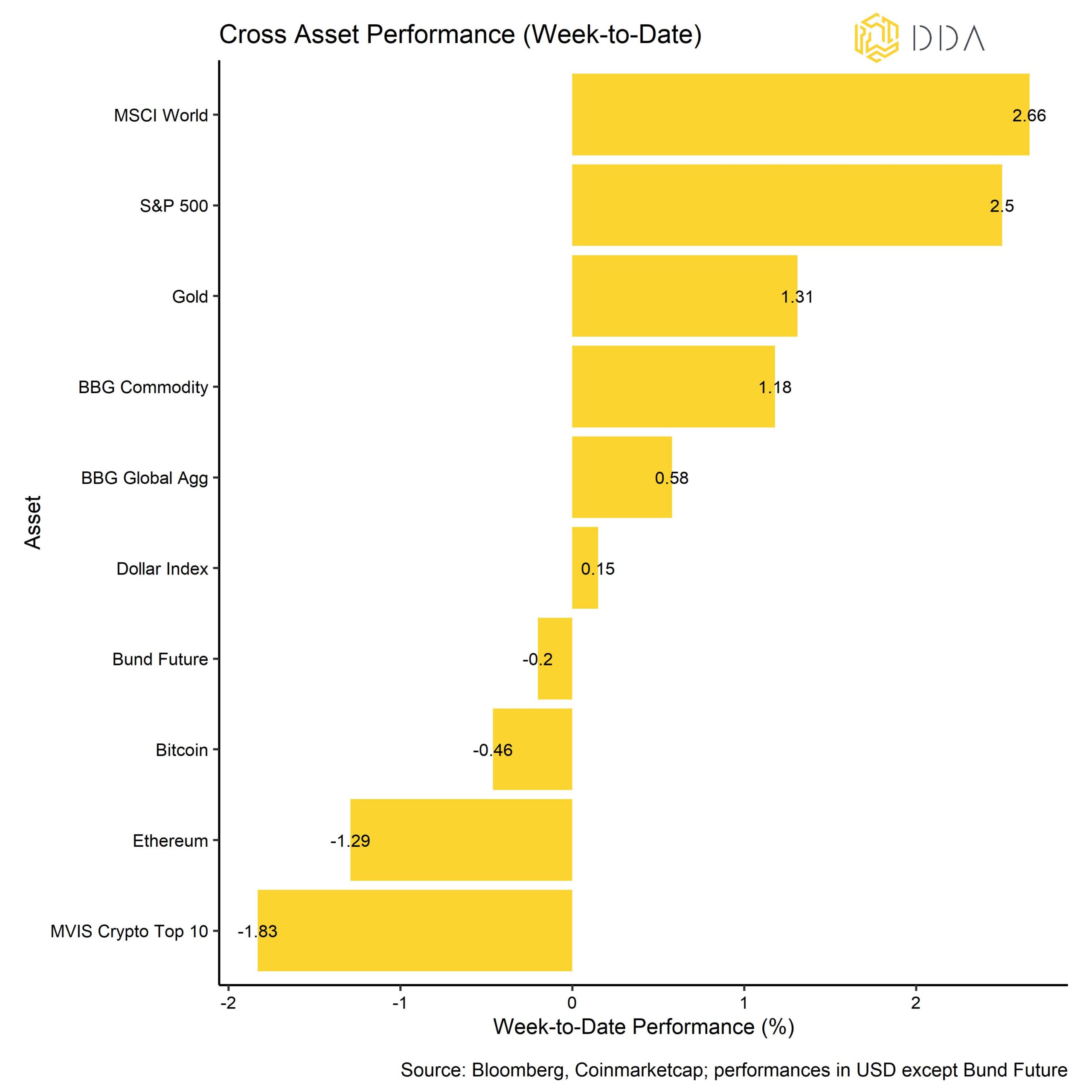

- Last week, cryptoassets posted a weak performance due to increasing selling pressure following the positive news relating to the potential approval of a US Bitcoin Spot ETF

- Our in-house Crypto Sentiment Index is still in bearish territory

- Bitcoin saw significant exchange inflows from whales that might have used the recent SEC related price surge as exit liquidity

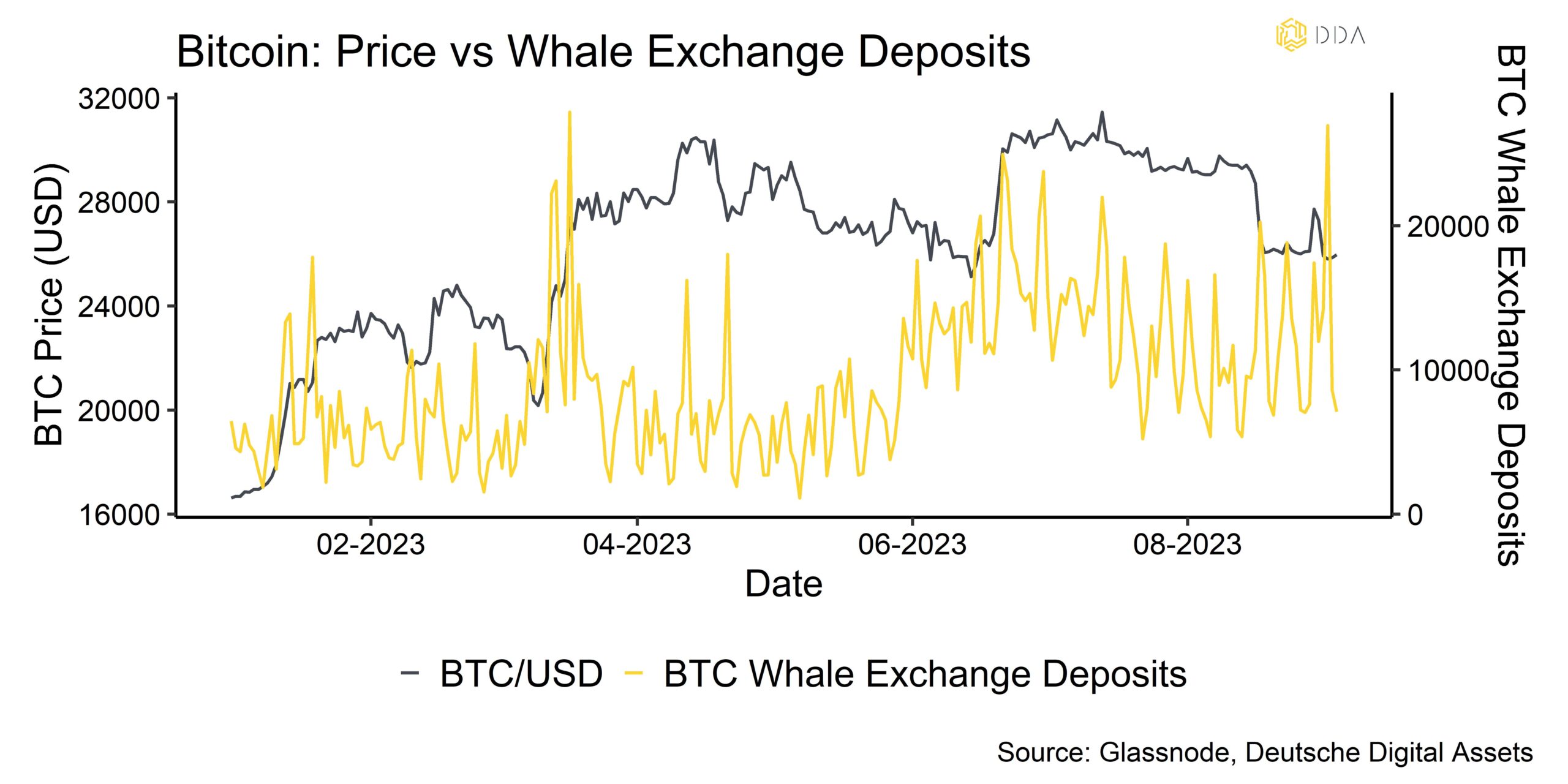

Chart of the week

Cryptoasset Performance

Last week, cryptoassets posted a weak performance due to increasing selling pressure following the positive news relating to a potential approval of a US Bitcoin Spot ETF. More specifically, the DC Circuit court soundly rejected the SEC’s view that Grayscale’s ETF proposal was not “designed to prevent fraudulent and manipulative acts and practices.” The court did not order the SEC to approve Grayscale’s ETF proposal. It just said the SEC’s analysis on the “fraud and manipulation” issue was wrong which means that the SEC needs to review Grayscale’s ETF application again.

However, Bloomberg analysts already point to a very high probability for the approval of a Bitcoin Spot ETF in the US. These kinds of news seem to be more than priced in. In this regard, Bitcoin saw significant exchange inflows from whales that might have used the recent Bitcoin ETF related price surge as exit liquidity. (Chart-of-the-Week).

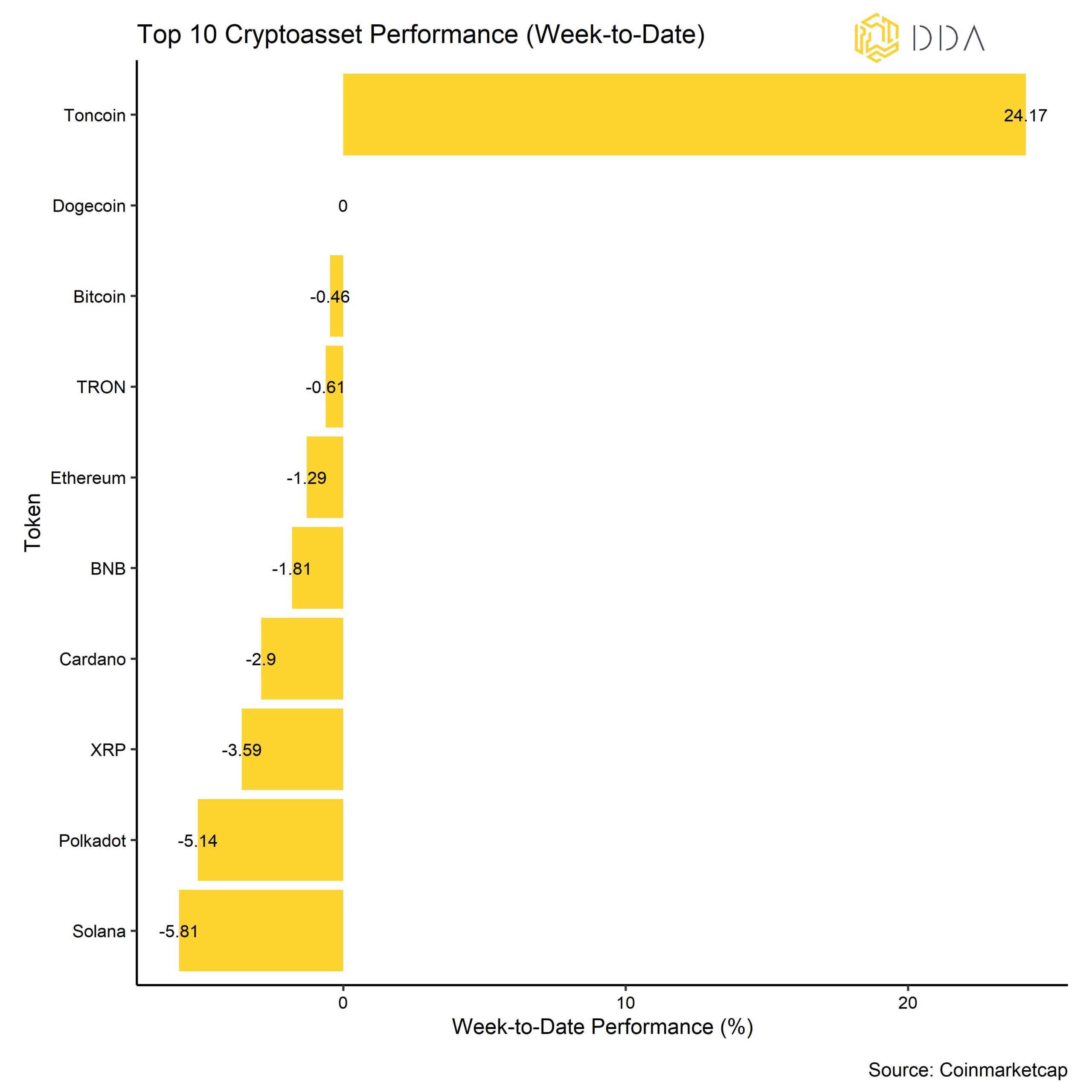

Among the top 10 cryptoassets, Toncoin, Dogecoin, and Bitcoin were the relative outperformers. Toncoin (TON) defied the overall bearish market sentiment as the token related to the messenger platform Telegram is rumoured to debut on Binance.

In general, altcoin outperformance vis-à-vis Bitcoin continued to be low last week. Based on our set of tracked altcoins only 30% of altcoins were able to outperform Bitcoin on a weekly basis.

Crypto Market Sentiment

Our in-house Crypto Sentiment Index decreased again compared to last week and firmly remains in bearish territory. Only 2 out of 15 indicators are above their short-term trend.

Compared to last week, we saw major reversals to the downside in the BTC Futures & Perpetual Positioning Proxy and Crypto Dispersion Index.

The Crypto Fear & Greed Index remains in “Fear” territory as of this morning.

Performance dispersion among cryptoassets has continued to decrease significantly since the liquidation event at the end of August.

In general, low performance dispersion among cryptoassets implies that correlations among cryptoassets is high which means that cryptoassets are trading more on systematic factors.

At the same time, as mentioned above, altcoin outperformance has continued to be low last week and is now at 30% of altcoins outperforming Bitcoin on a weekly basis.

In general, altcoin outperformance goes hand in hand with an increase in crypto dispersion, i.e. Bitcoin and altcoins are generally trading up during “altseason” with altcoins outperforming Bitcoin. Broader altcoin outperformance is usually a sign of increasing risk appetite and broader altcoin underperformance a sign of increasing risk aversion.

Crypto Asset Flows

Last week saw net outflows from global crypto ETPs except Bitcoin.

In aggregate, we saw net fund outflows in the amount of -21.8 mn USD (week ending Friday).

Accordingly, Ethereum funds and other Altcoin-based funds experienced significant net outflows (-16.9 mn USD and -8.8 mn USD on a net basis, respectively).

Thematic & basket crypto funds also experienced net outflows -2.5 mn USD last week.

In contrast, Bitcoin-based funds experienced net inflows (+6.5 mn USD).

Besides, the NAV discount of the biggest Bitcoin fund in the world – Grayscale Bitcoin Trust (GBTC) – has continued to narrow last week which implies net inflows into this fund vehicle. The narrowing NAV discount appears to be related to the expectation that this Trust is more likely to be converted into a Spot Bitcoin ETF.

Furthermore, the beta of global crypto hedge funds to Bitcoin over the last 20 trading days continued to be low, implying that global crypto hedge funds still have reduced market exposure to cryptoassets.

On-Chain Activity

Overall on-chain activity is less encouraging than a week ago although there still some positive green shots. For instance, active addresses on the Bitcoin blockchain have not yet recovered from the slide experienced at the end of August. However, new addresses have shown some resilience and remain at year-to-date highs. Besides, the Bitcoin hash rate is hovering near all-time highs as mining difficulty has surpassed a new all-time high as well. The number of addresses with non-zero balances has also continued to move higher.

Transfer volumes are still hovering at multi-year lows which currently aggravates market moves and volatility.

Meanwhile exchange balances continue to drop which implies continuing accumulation on a net basis. This is true both for Bitcoin (BTC) and Ethereum (ETH).

Recent BTC exchange inflows have been dominated by short-term holders and most of these flows had a loss bias, i.e. the majority of exchange inflows happened on account of realized losses.

It is important to note though that both long and short-term holders of Bitcoin have been realizing profits at an increasing scale. It seems as if investors are neutralizing their positions as they don’t expect the uptrend to continue for now.

It is also interesting to observe that mid-sized investors ($100k – $1M) have continued to withdraw coins from exchanges in significant size while larger wallets (> $1M) have been net depositors of coins to exchanges. In other words, there are opposing forces at present.In fact, whale deposits to exchanges have spiked to the highest levels since the SVB collapse in March 2023. Whales may have taken the recent price surge as ‘exit liquidity’ and sold into strength after the positive SEC news (Chart-of-the-Week). Whales are entities that control at least 1000 BTC.

Cryptoasset Derivatives

Last week, derivatives metrics showed some continuing market cleansing.

BTC long liquidations have risen in consequence of the recent sell-off but were not as pronounced as during the liquidation event in mid-August.

Open Interest both for BTC Futures and Perpetuals had increased in the run-up to the recent price decline and decreased with the renewed price decline again. This implies that most of the futures and perpetual long positions that had been built before the DC Circuit ruling have already been wiped out again.

Despite the recent market turbulence, BTC 1-month implied volatilities continued to decrease as option traders seem to expect a calmer market environment for Bitcoin going forward.

In the wake of the most recent price decline we saw a significant increase in BTC puts trading volumes relative to calls, so BTC option traders were increasingly bidding for downside protection. The relative open interest of puts versus calls also remains elevated. The 1-month 25-delta BTC option skew has also steepened significantly in favour of puts. In general, the BTC options market currently signals a bearish sentiment as well.

Meanwhile, the BTC 3-months basis rate continued to decrease and is now at around 3.9% p.a.

Bottom Line

Last week, cryptoassets posted a weak performance due to increasing selling pressure following the positive news relating to the potential approval of a US Bitcoin Spot ETF.

Our in-house Crypto Sentiment Index is still in bearish territory.

Bitcoin saw significant exchange inflows from whales that might have used the recent SEC related price surge as exit liquidity.

About Deutsche Digital Assets

Deutsche Digital Assets is the trusted one-stop-shop for investors seeking exposure to crypto assets. We offer a menu of crypto investment products and solutions, ranging from passive to actively managed exposure, as well as financial product white-labeling services for asset managers.

We deliver excellence through familiar, trusted investment vehicles, providing investors the quality assurances they deserve from a world-class asset manager as we champion our mission of driving crypto asset adoption. DDA removes the technical risks of crypto investing by offering investors trusted and familiar means to invest in crypto at industry-leading low costs.

Legal Disclaimer

The material and information contained in this article is for informational purposes only. Deutsche Digital Assets, its affiliates, and subsidiaries are not soliciting any action based upon such material. This article is neither investment advice nor a recommendation or solicitation to buy any securities. Performance is unpredictable. Past performance is hence not an indication of any future performance. You agree to do your own research and due diligence before making any investment decision with respect to securities or investment opportunities discussed herein. Our articles and reports include forward-looking statements, estimates, projections, and opinions. These may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond Deutsche Digital Assets GmbH’s control. We believe all information contained herein is accurate, reliable and has been obtained from public sources. However, such information is presented “as is” without warranty of any kind.