Trotz der Liquiditätskrise, mit der zentralisierte Krypto-Kreditunternehmen konfrontiert sind, haben dezentrale Finanzprotokolle (DeFi) dem Druck standgehalten und funktionieren weiterhin wie vorgesehen. Lesen Sie weiter, um mehr über den Unterschied zwischen DeFi und CeFi zu erfahren und warum das jüngste Drama im zentralisierten Krypto-Kreditsektor ein starkes Argument für dezentralisierte Finanzen ist.

CeFi vs. DeFi: Was ist der Unterschied?

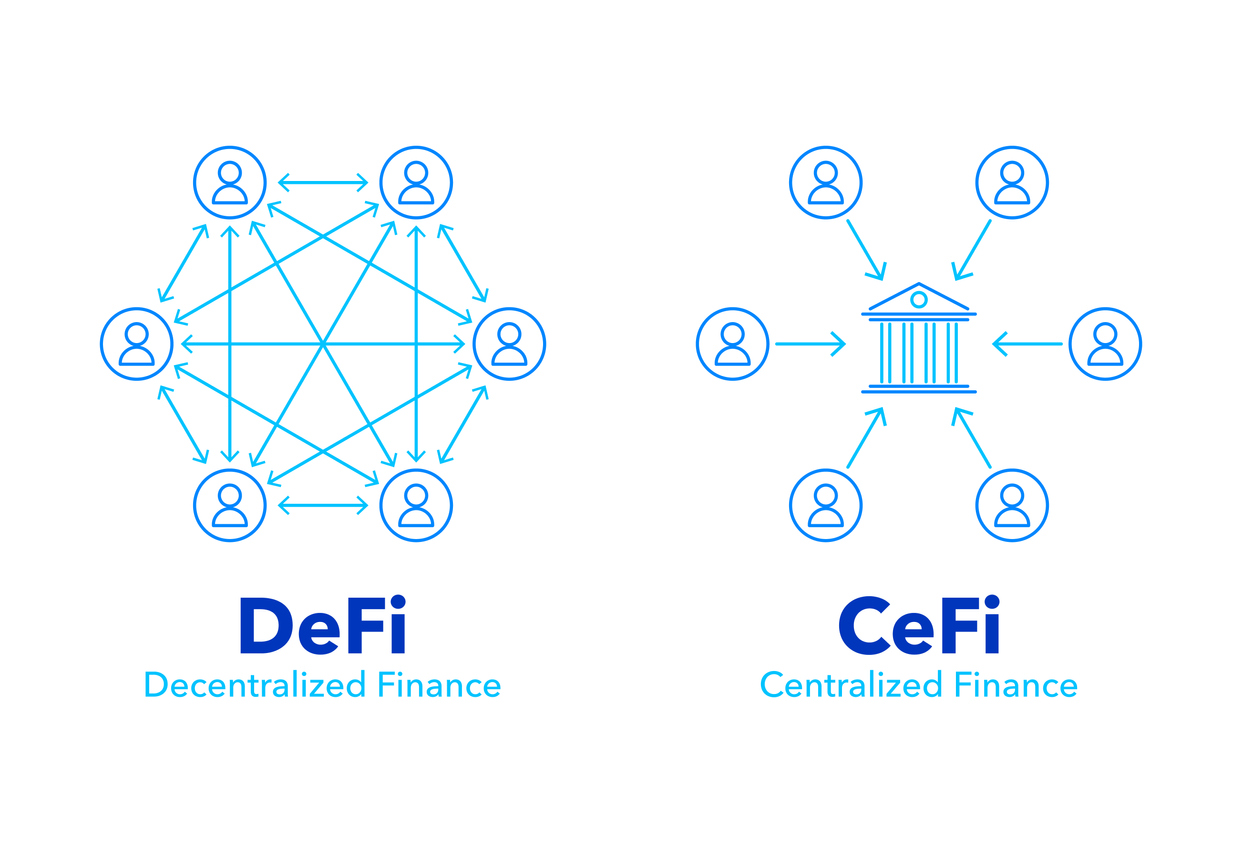

Traditionell wurden Finanzprodukte und -dienstleistungen von vertrauenswürdigen, zentralisierten Vermittlern wie Banken, Maklern und anderen Finanzinstituten angeboten.

Kryptowährungsunternehmen haben das gleiche Modell angewandt, um Dienstleistungen wie Handel, Investitionen und Kredite anzubieten. Auf den Kryptomärkten werden diese Unternehmen als zentralisierte Finanzanbieter (CeFi) bezeichnet. Krypto-Börsen und Krypto-Kreditplattformen sind Beispiele für CeFi-Unternehmen.

Im Gegensatz dazu ist das dezentrale Finanzwesen (DeFi) eine neue Reihe von internetbasierten Finanzprodukten und -dienstleistungen, die auf der Blockchain-Technologie beruhen. Anstelle zentraler Behörden, die als Vermittler fungieren, werden DeFi-Protokolle von intelligenten Verträgen betrieben und laufen autonom, um die Notwendigkeit einer einzigen Instanz zur Abwicklung von Transaktionen zu verringern.

Während die meisten führenden DeFi-Plattformen von Unternehmen unterstützt werden, die den Code des Protokolls entwickeln und pflegen, kann die DeFi-Anwendung nach ihrer Bereitstellung in der Regel nur mit Zustimmung der Protokoll-Community geändert werden.

Die Gemeinschaft besteht in der Regel aus den Inhabern von Protokoll-Token, die eine DAO (dezentrale autonome Organisation) bilden und über die von den Mitgliedern eingereichten Vorschläge abstimmen.

Der Hauptunterschied zwischen CeFi und DeFi besteht darin, dass bei CeFi das Vertrauen bei den zentralen Stellen verbleibt, während DeFi ohne Vertrauen arbeitet, da die gesamte Funktionsweise der dezentralen Finanzanwendungen auf der Kette eingesehen werden kann.

CeFi vs. DeFi Lending: Ein Vergleich

CeFi und DeFi Kredit- und Darlehensplattformen haben beide ihre Vor- und Nachteile. Schauen wir uns die beiden Arten von Krypto-Lending-Ansätzen an und wie sie sich vergleichen.

| CeFi Kreditvergabe | DeFi Kreditvergabe |

| zahlt in der Regel hohe Zinssätze | zahlt in der Regel niedrigere Zinssätze |

| Einhaltung einiger Vorschriften | Weitgehend unreguliert (mit null Verbraucherschutz) |

| On-Rampe von Fiat zu Krypto (ermöglicht Einzahlungen in Fiat-Währung) | Nutzer können nur Krypto-Assets tauschen, leihen und verleihen |

| Geringeres technisches Risiko, da Intermediäre die Kreditvergabe erleichtern | Intelligente Verträge können Bugs haben, die Hacker ausnutzen können |

| Nutzer müssen ein Konto registrieren und auf die KYC-Genehmigung warten, bevor sie die Dienste einer Plattform nutzen können | Keine KYC- oder ID-Dokumentation erforderlich |

| Vermögensverwahrung liegt in den Händen der Krypto-Plattform | Die Nutzer haben das volle Sorgerecht für ihr Vermögen |

| Der zentralisierte Entscheidungsprozess über die Verwendung der Gelder der Kreditgeber kann zu Undurchsichtigkeit führen | Äußerst transparent, da alles auf der Kette passiert |

| Die Darlehensgenehmigung unterliegt einer KYC/AML-Überprüfung | Keine Bonitätsprüfung erforderlich |

| Kreditnehmer können einen Arbeitstag oder länger auf die Kreditgenehmigung warten | Kreditnehmer können Kredite innerhalb von Minuten sichern |

Wie Sie aus der obigen Tabelle ersehen können, ist es schwierig zu behaupten, dass die eine besser ist als die andere, denn beide haben klare Vor- und Nachteile.

Was wir jedoch in Q2/2022 auf dem zentralisierten Krypto-Kreditmarkt gesehen haben, deutet darauf hin, dass die Zukunft der Kreditvergabe für digitale Vermögenswerte wahrscheinlich auf dezentralen Protokollen beruhen sollte, die nicht für die gleichen Probleme anfällig sind wie die traditionelle Finanzindustrie.

Was ist in der zentralisierten Krypto-Kreditlandschaft passiert?

Nach der Zusammenbruch von Terra (LUNA) und TerraUSD (UST)Zahlreiche zentralisierte Krypto-Kreditgeber, die in diesen beiden Vermögenswerten engagiert waren (oder Gegenparteien mit Engagement), erlebten eine Liquiditätskrise, die zu Konkursen und Rettungsaktionen führte.

Zunächst stoppten eine Handvoll Krypto-Kreditgeber die Abhebungen ihrer Kunden, um sicherzustellen, dass sie liquide bleiben und ihren Verpflichtungen nachkommen konnten. Es wurde jedoch bald klar, dass der Zusammenbruch des Terra-Ökosystems diese Kreditgeber treffen und zu Firmenzusammenbrüchen führen würde.

Während einige Kreditgeber das Glück hatten, von kapitalkräftigen Kryptounternehmen de facto gerettet zu werden, mussten andere ihre Türen schließen und ließen die Einleger mit leeren Händen zurück.

Aber wie konnten zahlreiche führende Krypto-Kreditgeber scheitern, nur weil zwei Kryptowährungen zusammengebrochen sind?

Die Antwort liegt in der Art und Weise, wie diese Kreditgeber operierten, um die hohen Zinsen zu erzielen, die sie den Einlegern zahlen konnten.

Wenn ein Kryptoanleger Gelder auf einer zentralen Kreditplattform einzahlte, verlieh der Dienstleister diese Gelder an große Kryptokreditnehmer. Bei diesen Kreditnehmern handelte es sich in der Regel um Hedgefonds oder große VC-Unternehmen, die das geliehene Kapital in hochrentable Krypto-Investitionsstrategien investierten.

Einige kauften zum Beispiel UST und legten sie in Anchor Protocol an, das 20% APY zahlte. Andere investierten in LUNA oder andere digitale Vermögenswerte, von denen sie glaubten, dass sie das Potenzial hätten, ihren Wert erheblich zu steigern.

Das Problem trat auf, als große Kreditnehmer den kreditgebenden Unternehmen keine Rückzahlungen mehr leisten konnten, da sie erhebliche Summen in LUNA und UST oder anderen Anlagen verloren hatten. Infolgedessen konnten die Kreditgeber die Einleger nicht mehr auszahlen, weil die Kreditnehmer ihnen die Rückzahlung versagten.

Darüber hinaus haben einige Darlehensgeber Berichten zufolge auch Kundengelder in renditestarke Krypto-Investitionsmöglichkeiten investiert und damit im Grunde genommen ohne Wissen oder Zustimmung ihrer Kunden ein zu hohes Risiko mit Kundengeldern eingegangen sind.

Als schließlich die Liquiditätskrise auf den Kreditmärkten offensichtlich wurde, fiel der Markt für Kryptowährungen aufgrund von Zwangsverkäufen und einer negativen Anlegerstimmung erheblich.

Infolgedessen konnten die Gegenparteien, die den Kreditgebern Geld schuldeten, nicht genügend Vermögenswerte zu einem angemessenen Preis verkaufen, um ihre Kreditverpflichtungen zu erfüllen. Dadurch fehlten den Kreditgebern die Mittel, um ihren Verpflichtungen gegenüber den Einlegern nachzukommen.

Die Liquiditätskrise auf den zentralisierten Krypto-Kreditmärkten ist im Wesentlichen darauf zurückzuführen, dass große Akteure der Branche sich gegenseitig Geld leihen und verleihen. Als der Markt nach dem Zusammenbruch von Terra und UST ins Wanken geriet, führte die Verflechtung dieser großen Akteure zu einem kaskadenartigen Ausfall von Gegenparteien.

Warum DeFi Lending dem Sturm standgehalten hat

Während der zentrale Krypto-Kreditmarkt durch den Zusammenbruch von Luna (LUNA) und TerraUSD (UST) erschüttert wurde, was zu einer Reihe von Konkursen und Rettungsaktionen von Kreditgebern führte, funktionierte der dezentrale Krypto-Kreditmarkt weiterhin ohne Probleme.

Die Kreditkrise auf dem zentralisierten Kreditmarkt hatte keine Auswirkungen auf die DeFi-Kreditprotokolle, da die Kreditnehmer ihre Kredite überbesichern. Wenn Kreditnehmer bei DeFi die Sicherheiten nicht über die Nachschussforderung hinaus aufrechterhalten können, werden sie vom intelligenten Vertrag liquidiert. Dadurch wird verhindert, dass die Einleger (Kreditgeber) ihr Geld verlieren.

DeFi-Plattformen praktizieren ein gesundes Risikomanagement; die meisten von ihnen haben einen Mindestbeleihungsauslauf (LTV) von etwa 60 bis 90%. Zum Beispiel haben Stablecoins auf Aave einen LTV von 75%, während der LTV anderer Vermögenswerte zwischen 15-60% liegt.

Außerdem bedeutet das Fehlen von Vermittlern, dass DeFi-Kreditprotokolle das Geld der Einleger nicht in Strategien investieren können, die sie nicht genehmigt haben. Außerdem bevorzugen die Smart-Contract-Regeln keine bestimmten Kreditnehmer gegenüber anderen. Niemand kann aufgrund seiner Reputation eine Vorzugsbehandlung erhalten (wie es auf dem zentralisierten Krypto-Kreditmarkt der Fall war).

Bei DeFi muss jeder Kreditnehmer seinen Kredit überbesichern und über dem Margenausgleich halten. Geschieht dies nicht, wird er liquidiert. Die Regeln sind klar und können nicht geändert werden. Die Blockchain-Technologie sorgt dafür, dass die DeFi-Kreditprotokolle transparent und nachvollziehbar bleiben.

Aus diesen Gründen hat DeFi in der jüngsten Baisse besser abgeschnitten als CeFi, was die Stärke von kryptobasierten, dezentralen Finanzdienstleistungen unterstreicht.

Über DDA Ikonische Fonds

Iconic Funds ist die Brücke zu Krypto-Investitionen durch vertrauenswürdige Anlageinstrumente. Wir bieten Anlegern sowohl passive als auch Alpha-Strategien für Kryptowährungen sowie Risikokapitalmöglichkeiten.

Wir liefern hervorragende Leistungen durch vertraute, regulierte Vehikel, die den Anlegern die Qualitätsgarantien bieten, die sie von einem erstklassigen Vermögensverwalter erwarten, während wir unsere Mission verfolgen, die Verbreitung von Kryptoanlagen voranzutreiben.

Aktuelle Nachrichten und Artikel

- Das Argument für aktiv verwaltete Anlagestrategien auf den Kryptomärkten

- Iconic startet aktiv verwaltete Krypto-Anlageplattform mit dem kürzlich erworbenen Quantitative Solutions Team

- Wie man in NFTs investiert: Ein Leitfaden für professionelle Anleger

- Bitcoin vs. Gold: Warum Sie wahrscheinlich besser dran sind, wenn Sie "digitales Gold" kaufen

- Warum die Volatilität von Bitcoin Sie nicht erschrecken sollte

- Wie genau ist das Bitcoin Stock-to-Flow-Modell?

Iconic in der Presse

- ETF-Stream: Zahl der White-Label-Emittenten in Europa innerhalb einer Woche verdreifacht

- ETF-Strategie: Iconic Funds lanciert das weltweit erste Krypto-ETP auf ApeCoin

- Das Investment: Kryptowährungen kommen 2022 im Mainstream an

- Private Banking Magazin, Bitcoin - das perfekte Beispiel für ein ESG-Investment?

- Institutionelles Geld, Krypto-Manager steigt bei Family Office ein

- Morningstar, Iconic Funds erweitert seine Produktpalette mit einem physischen Ethereum-ETP

Aktuelle Forschungsberichte

Wie haben sich die Portfolios während der Pandemie entwickelt? ➡ Hier herunterladen

Analyse der wichtigsten Werttreiber der führenden Kryptowährungen ➡ Hier herunterladen

Wie effektiv sind gängige Anlagestrategien mit Bitcoin? ➡ Hier herunterladen

Untersuchung des Mythos der Nullkorrelation zwischen Kryptowährungen und Marktindizes ➡ Hier herunterladen

Weitere Informationen finden Sie unter deutschedastg

Haftungsausschluss

Die in diesem Artikel enthaltenen Materialien und Informationen dienen ausschließlich zu Informationszwecken. Die Iconic Holding GmbH, ihre verbundenen Unternehmen und Tochtergesellschaften fordern nicht zu Handlungen auf der Grundlage dieses Materials auf. Dieser Artikel ist weder eine Anlageberatung noch eine Empfehlung oder Aufforderung zum Kauf von Wertpapieren. Die Wertentwicklung ist unvorhersehbar. Die Wertentwicklung in der Vergangenheit ist daher kein Hinweis auf die zukünftige Wertentwicklung. Sie erklären sich damit einverstanden, Ihre eigenen Nachforschungen anzustellen und Ihre Sorgfaltspflicht zu erfüllen, bevor Sie eine Anlageentscheidung in Bezug auf die hier besprochenen Wertpapiere oder Anlagemöglichkeiten treffen. Unsere Artikel und Berichte enthalten zukunftsgerichtete Aussagen, Schätzungen, Projektionen und Meinungen. Diese können sich als wesentlich ungenau erweisen und unterliegen erheblichen Risiken und Unwägbarkeiten, die außerhalb der Kontrolle der Iconic Holding GmbH liegen. Wir gehen davon aus, dass alle hierin enthaltenen Informationen korrekt und zuverlässig sind und aus öffentlichen Quellen stammen. Diese Informationen werden jedoch "wie besehen" und ohne jegliche Garantie präsentiert.