von André DragoschLeiter der Forschung

Wichtigste Erkenntnisse

- Die Wertentwicklung von Kryptowährungen war überwiegend negativ, was auf technische Faktoren und eine verstärkte regulatorische Kontrolle der Kryptoindustrie in den USA zurückzuführen ist

- Unser hauseigener Crypto Sentiment Index ist in der letzten Woche weiter gesunken, da der kurzfristige Überschwang weiter abnimmt

- Die Geldstrafe der SEC gegen den Börsenbetreiber Kraken erhöht die regulatorische Unsicherheit in den USA in Bezug auf Ethereum und Proof-of-Stake-Kryptoassets

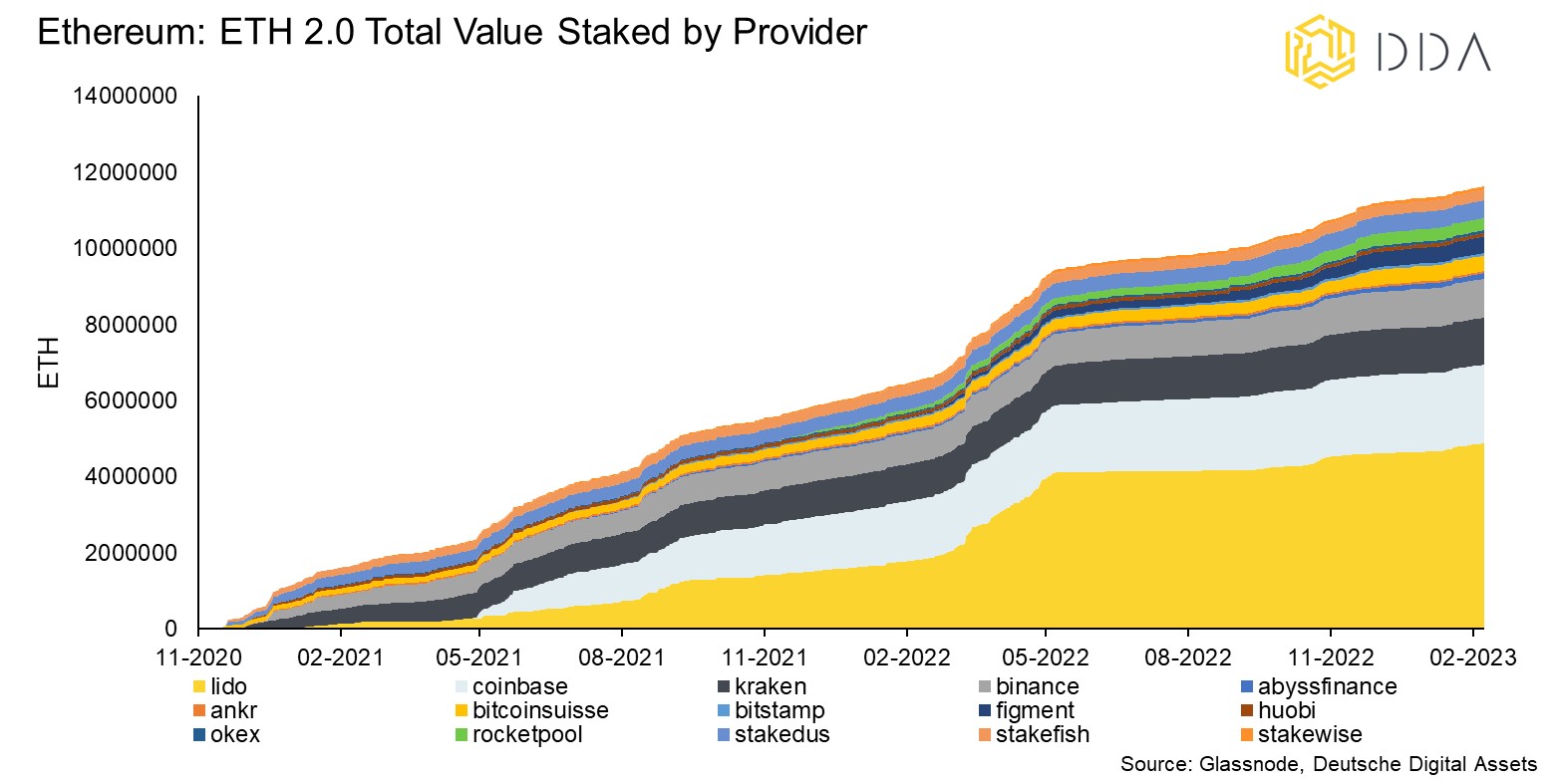

Chart der Woche

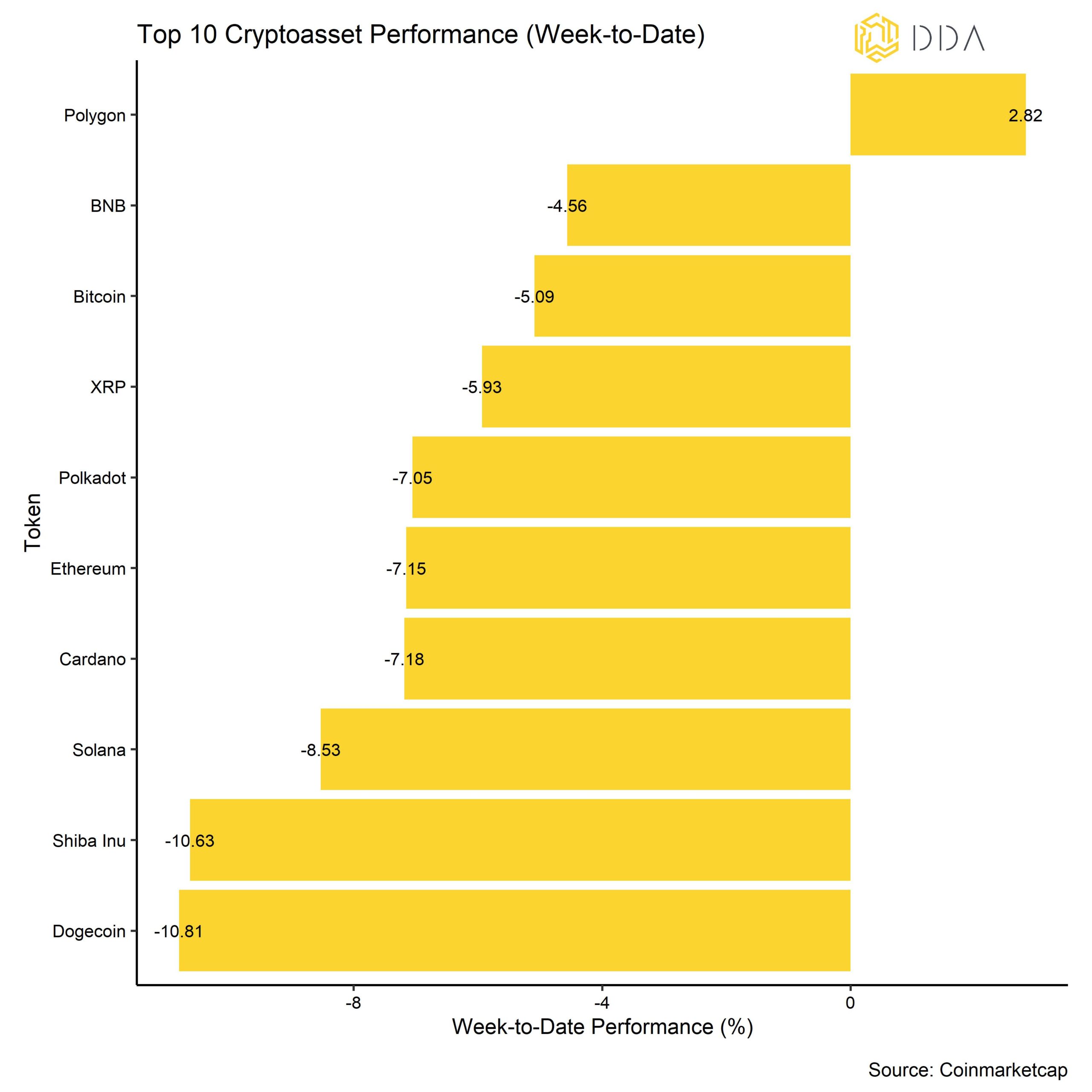

Kryptoasset Leistung

In der vergangenen Woche war die Performance von Kryptoassets überwiegend negativ, was auf technische Faktoren und eine verstärkte regulatorische Kontrolle der Kryptoindustrie in den USA zurückzuführen ist.

Ein wichtiger positiver Katalysator für die negative Entwicklung war die Tatsache, dass die SEC den Kryptobörsenbetreiber Kraken wegen seines "Staking-as-a-Service"-Angebots mit einer Geldstrafe von 30 Mio. USD belegt hat. Dies hat allgemein die regulatorische Unsicherheit in den USA in Bezug auf Ethereum und Proof-of-Stake-Kryptoassets erhöht.

Unter den wichtigsten Kryptoassets waren Polygon, BNB und Bitcoin die relativen Outperformer.

Die Gesamt-Outperformance von Altcoins bleibt jedoch gering, wenn man unseren hauseigenen "Altseason-Index" zugrunde legt, der die Outperformance von Altcoins gegenüber Bitcoin in den letzten drei Monaten verfolgt. Gleichzeitig scheinen Kryptoassets eher von münzspezifischen Faktoren als von systemischen Faktoren getrieben zu sein, wenn man die relativ hohe statistische Streuung zwischen den Kryptoassets betrachtet, auch wenn die Streuung in letzter Zeit leicht abgenommen hat.

Stimmung

Unser hauseigener Krypto-Sentiment-Index ist im Vergleich zur letzten Woche weiter gesunken, befindet sich aber immer noch im positiven Bereich. 11 von 15 Indikatoren liegen immer noch über ihrem kurzfristigen Trend. Nichtsdestotrotz waren die Umkehrungen in der letzten Woche recht ausgeprägt.

Wir sahen große Umschwünge bei den BTC-Finanzierungsraten für unbefristete Futures-Kontrakte sowie beim Verhältnis zwischen Put- und Call-Volumen für Bitcoin-Optionen, da die Händler begannen, mehr für Put-Optionen als für Calls zu bieten. Auch bei den On-Chain-Indikatoren gab es einige größere Umschwünge.

Der Crypto Fear & Greed Index kehrte ebenfalls von "Greed" in den "neutralen" Bereich zurück. Die auf Bitcoin Twitter gemessene Stimmung blieb während der gesamten letzten Woche bärisch.

Wie bereits erwähnt, war die Streuung zwischen den Kryptoassets weiterhin hoch, obwohl sie in letzter Zeit ebenfalls abgenommen hat. Gleichzeitig entwickelten sich Altcoins auf 1-Monats- und 3-Monats-Basis meist schlechter als Bitcoin. Auf 1-Monats-Basis haben nur 15% der erfassten Altcoins eine bessere Performance als Bitcoin erzielt. Eine Outperformance von Altcoins ist in der Regel ein Zeichen für eine erhöhte Risikobereitschaft, und eine geringe Outperformance von Altcoins ist derzeit ein Hinweis auf eine eher vorsichtige Marktstimmung.

Strömungen

In der vergangenen Woche scheinen die Zuflüsse in Kryptoassets und insbesondere in Bitcoin-Fonds nachgelassen zu haben.

Insgesamt verzeichneten wir Netto-Fondsabflüsse in Höhe von -32,3 Mio. USD. Die Abflüsse konzentrierten sich vor allem auf BTC-basierte Produkte (-25,8 Mio. USD) und Basket & Thematics-Produkte (-14,1 Mio. USD). Im Gegensatz dazu verzeichneten Altcoin-basierte Produkte während der gesamten Woche Nettozuflüsse (ETH +3,6 Mio. USD und Altcoins ex ETH +4,0 Mio. USD), obwohl es sich dabei wahrscheinlich eher um eine Aufholjagd gegenüber der Vorwoche handelt.

In diesem Zusammenhang ist der Abschlag auf den Nettoinventarwert des größten Bitcoin-Fonds der Welt - Grayscale Bitcoin Trust (GBTC) - erneut gesunken, was darauf hindeutet, dass die institutionelle Nachfrage weiter zurückgegangen ist.

Das Beta der globalen Hedge-Fonds gegenüber Bitcoin ist in den letzten 20 Handelstagen weiter leicht gesunken, was bedeutet, dass Hedge-Fonds ihr Engagement in Krypto-Assets in den letzten 20 Tagen weiter reduziert haben könnten.

Die auf Coinbase gehandelten Bitcoin-Preise waren im Vergleich zu den auf Binance gehandelten (Coinbase-Binance-Prämie) während der gesamten Woche weitgehend unverändert, was auf ein neutrales Kaufinteresse von institutionellen Anlegern gegenüber Kleinanlegern hindeutet.

On-Chain

Die Geldstrafe der SEC gegen den Börsenbetreiber Kraken hat die regulatorische Unsicherheit in den USA in Bezug auf Ethereum und Proof-of-Stake-Kryptoassets erhöht.

Derzeit sind rund 1,2 Mio. ETH über Kraken gestapelt, was den drittgrößten Pool an gestapeltem Ethereum darstellt. Coinbase und Binance beherbergen weitere 2,06 Mio. ETH und 1,01 Mio. ETH an gestapeltem Ethereum auf ihren Börsen, wie in unserem Chart-der-Woche.

Diese eingesetzten ETH laufen Gefahr, von diesen Börsen abgezogen zu werden, sobald das bevorstehende "Shanghai-Upgrade" den Validierern erlaubt, ihr eingesetztes Ethereum abzuziehen, was derzeit nicht möglich ist. Es wird erwartet, dass dies irgendwann im März oder April dieses Jahres möglich sein wird.

Das Verfahren der SEC gegen "Staking-as-a-Service"-Anbieter wie Kraken kommt zu einer Zeit, in der Kryptoexperten in den USA kürzlich vor einem möglichen Durchgreifen gegen die Branche gewarnt haben, die kürzlich als "Operation Chokepoint 2.0". Wir sollten also in den kommenden Wochen generell mit mehr negativen Nachrichten in Bezug auf die US-Krypto-Regulierung rechnen.

Aufgrund der erhöhten regulatorischen Unsicherheit haben wir in letzter Zeit einen Anstieg der Ethereum-Börsenabflüsse beobachtet, insbesondere am Freitag letzter Woche, als die höchsten Abflüsse seit Dezember letzten Jahres verzeichnet wurden. Im Gegensatz dazu gab es bei Bitcoin keine ungewöhnlichen Börsenaktivitäten, obwohl wir einen leichten Anstieg der Wal-Börseneinlagen sahen, die in der Regel auf ein erhöhtes Verkaufsvolumen durch Großinvestoren hinweisen.

Ein weiterer Aspekt ist, dass die kurzfristigen Händler anscheinend wieder Verluste hinnehmen müssen, wenn man das negative STH-SOPR-Verhältnis (Short-term Holder Spent-Output-Profit Ratio) betrachtet. Dies könnte kurzfristig zu mehr Volatilität auf dem Markt führen, da die Händler eher geneigt sein könnten, ihre Positionen zu verkaufen. Insgesamt bleiben die kurzfristigen Händler jedoch in der Gewinnzone, gemessen an der STH-NUPL-Metrik.

Derivate

Im Allgemeinen hat der höhere Grad an Unsicherheit noch nicht zu einem Anstieg der Risikoaversion an den Derivatemärkten geführt. Die implizite Volatilität von 1-Monats-Bitcoin-Optionen ist weiter gesunken, was auf einen Rückgang der Risikoaversion unter Optionshändlern schließen lässt. Der 25-Delta-Skew hat sich jedoch in letzter Zeit verringert und ist nun wieder negativ, was bedeutet, dass Optionshändler Verkaufsoptionen höher bewerten als delta-äquivalente Kaufoptionen. Obwohl das Verhältnis zwischen Verkaufsund Kaufvolumen in letzter Zeit zugenommen hat, sind die Händler von Bitcoin-Optionen, gemessen am relativen offenen Interesse, weiterhin fest in Kaufoptionen positioniert.

Andererseits sind sowohl die Bitcoin-Perpetual-Funding-Sätze als auch der Futures-Basissatz in letzter Zeit gesunken, was darauf hindeutet, dass die Nachfrage nach Short-Kontrakten im Vergleich zu Long-Kontrakten in letzter Zeit wieder zugenommen hat.

Unterm Strich

Die Performance von Kryptoassets war überwiegend negativ, was auf technische Faktoren und eine verstärkte regulatorische Kontrolle der Kryptoindustrie in den USA zurückzuführen ist.

Unser hauseigener Krypto-Sentiment-Index ist in der vergangenen Woche weiter gesunken, da der kurzfristige Überschwang weiter abnimmt.

Die Geldstrafe der SEC gegen den Börsenbetreiber Kraken erhöht die regulatorische Unsicherheit in den USA in Bezug auf Ethereum und Proof-of-Stake-Kryptoassets.

Über DDA Deutsche Digital Assets

Deutsche Digital Assets (DDA) ist ein deutscher Digital Asset Manager, der als vertrauenswürdige Anlaufstelle für Investoren dient, die ein Exposure zu Krypto Assets suchen. Über verschiedene Tochtergesellschaften bietet DDA eine Reihe von kryptobezogenen Anlageprodukten an, die von passiven bis hin zu aktiv verwalteten Investmentlösungen reichen. Darüber hinaus bietet das Unternehmen professionelle Anlageberatung für Family Offices, High Net Worth Individuals (HNWI) und institutionelle Anleger an.

Wir bieten hervorragende Leistungen durch vertraute, vertrauenswürdige Anlagevehikel, die den Anlegern die Qualitätsgarantien bieten, die sie von einem erstklassigen Vermögensverwalter verdienen, während wir uns für unsere Mission einsetzen, die Akzeptanz von Kryptoanlagen zu fördern. DDA beseitigt die technischen Risiken von Krypto-Investitionen, indem wir Anlegern vertrauenswürdige und vertraute Mittel zur Investition in Krypto zu branchenführend niedrigen Kosten anbieten.

Haftungsausschluss

Die in diesem Artikel enthaltenen Materialien und Informationen dienen ausschließlich zu Informationszwecken. Die Deutsche Digital Assets, ihre verbundenen Unternehmen und Tochtergesellschaften fordern nicht zu Handlungen auf der Grundlage dieses Materials auf. Dieser Artikel ist weder eine Anlageberatung noch eine Empfehlung oder Aufforderung zum Kauf von Wertpapieren. Die Wertentwicklung ist unvorhersehbar. Die Wertentwicklung in der Vergangenheit ist daher kein Hinweis auf die zukünftige Wertentwicklung. Sie erklären sich damit einverstanden, Ihre eigenen Nachforschungen anzustellen und Ihre Sorgfaltspflicht zu erfüllen, bevor Sie eine Anlageentscheidung in Bezug auf die hier besprochenen Wertpapiere oder Anlagemöglichkeiten treffen. Unsere Artikel und Berichte enthalten zukunftsgerichtete Aussagen, Schätzungen, Projektionen und Meinungen. Diese können sich als wesentlich ungenau erweisen und unterliegen erheblichen Risiken und Unwägbarkeiten, die außerhalb der Kontrolle der Deutsche Digital Assets GmbH liegen. Wir gehen davon aus, dass alle hierin enthaltenen Informationen korrekt und zuverlässig sind und aus öffentlichen Quellen stammen. Diese Informationen werden jedoch "wie besehen" und ohne jegliche Garantie präsentiert.