Erleichterung der Schuldenobergrenze sorgt für positives Momentum: Krypto-Sentiment-Index steigt, während institutionelle Käufer die Preise stabilisieren

DDA Krypto-Marktimpuls, 30. Mai 2023

von André DragoschLeiter der Forschung

Wichtigste Erkenntnisse

- Die Kryptoasset-Preise bewegten sich vor dem Erlass der Schuldenobergrenze, der vorerst als positiver Katalysator zu wirken scheint, überwiegend seitwärts

- Unser hauseigener Crypto Sentiment Index ist in der letzten Woche wieder gestiegen

- Einige institutionelle Käufer von Bitcoin scheinen die Preise zu drücken, wie die erheblichen Abflüsse in letzter Zeit zeigen

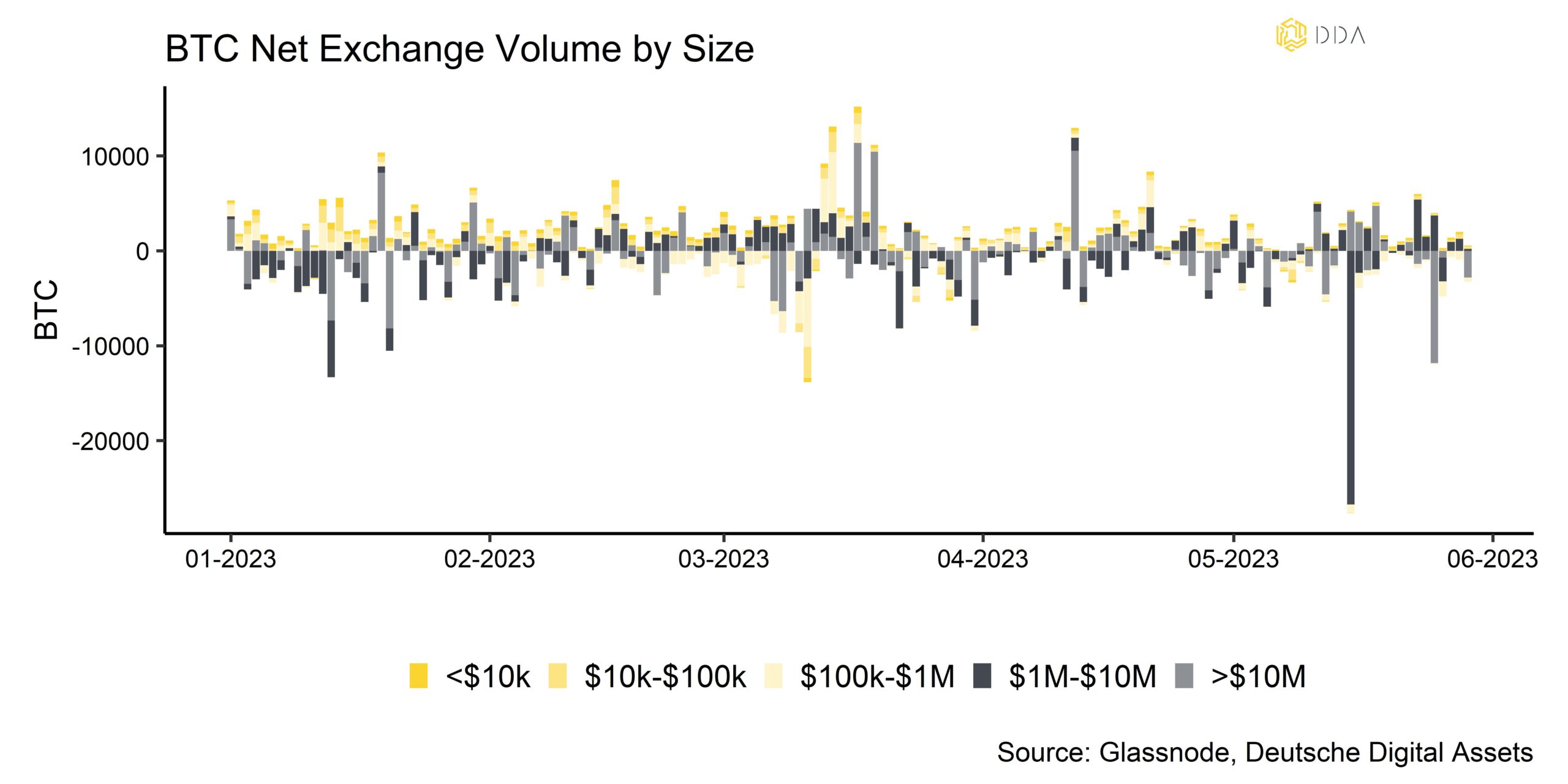

Chart der Woche

Kryptoasset Leistung

In der vergangenen Woche bewegten sich die Kryptoasset-Preise überwiegend seitwärts, bevor die Erleichterung der Schuldenobergrenze vorerst als positiver Katalysator zu wirken scheint. Die US-Gesetzgeber einigten sich auf eine Verlängerung der Schuldenobergrenze um ca. 4 Billionen USD auf ~35,4 Billionen USD bis Januar 2025 und stimmten Ausgabenkürzungen in Höhe von (nur) ca. 50 Mrd. USD zu.

Obwohl viele Ökonomen vor den möglichen negativen Auswirkungen auf die Gesamtliquidität durch eine Auffüllung des Treasury General Account (TGA) bei der Fed gewarnt haben, haben die Märkte bisher positiv auf die Nachricht reagiert.

Gleichzeitig scheinen einige institutionelle Bitcoin-Käufer die Preise unter Druck gesetzt zu haben, wie die erheblichen Abflüsse in letzter Zeit zeigen (Chart-der-Woche). Im Allgemeinen ist der Grad der Akkumulationsaktivität bei den verschiedenen Geldbörsenkohorten sehr hoch.

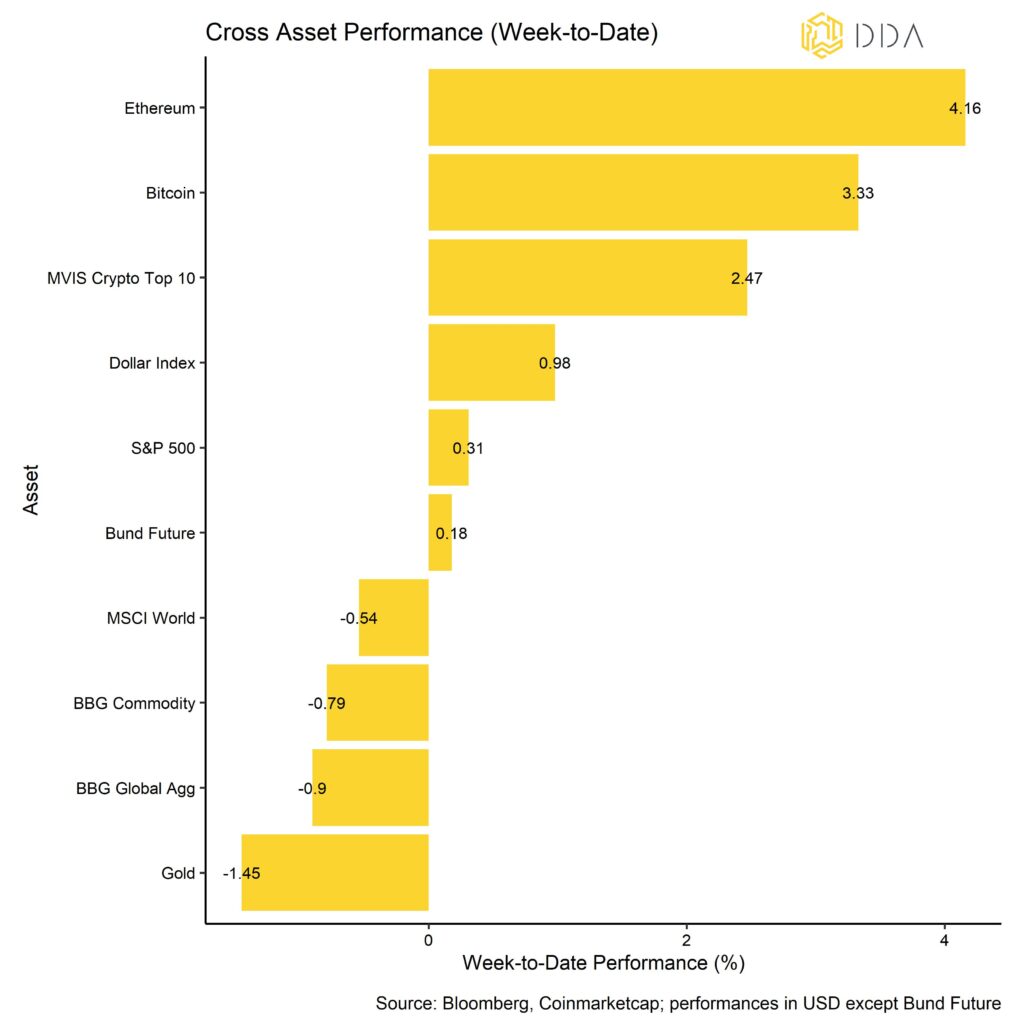

Alles in allem waren Kryptoanlagen in der vergangenen Woche die Anlageklasse mit der besten Performance. Während Kryptoassets zulegten, mussten globale Aktien, globale Anleihen und sogar Rohstoffe Rückschläge hinnehmen. Gold war der Vermögenswert mit der schlechtesten Performance, während der Dollar in der vergangenen Woche an Wert zulegte.

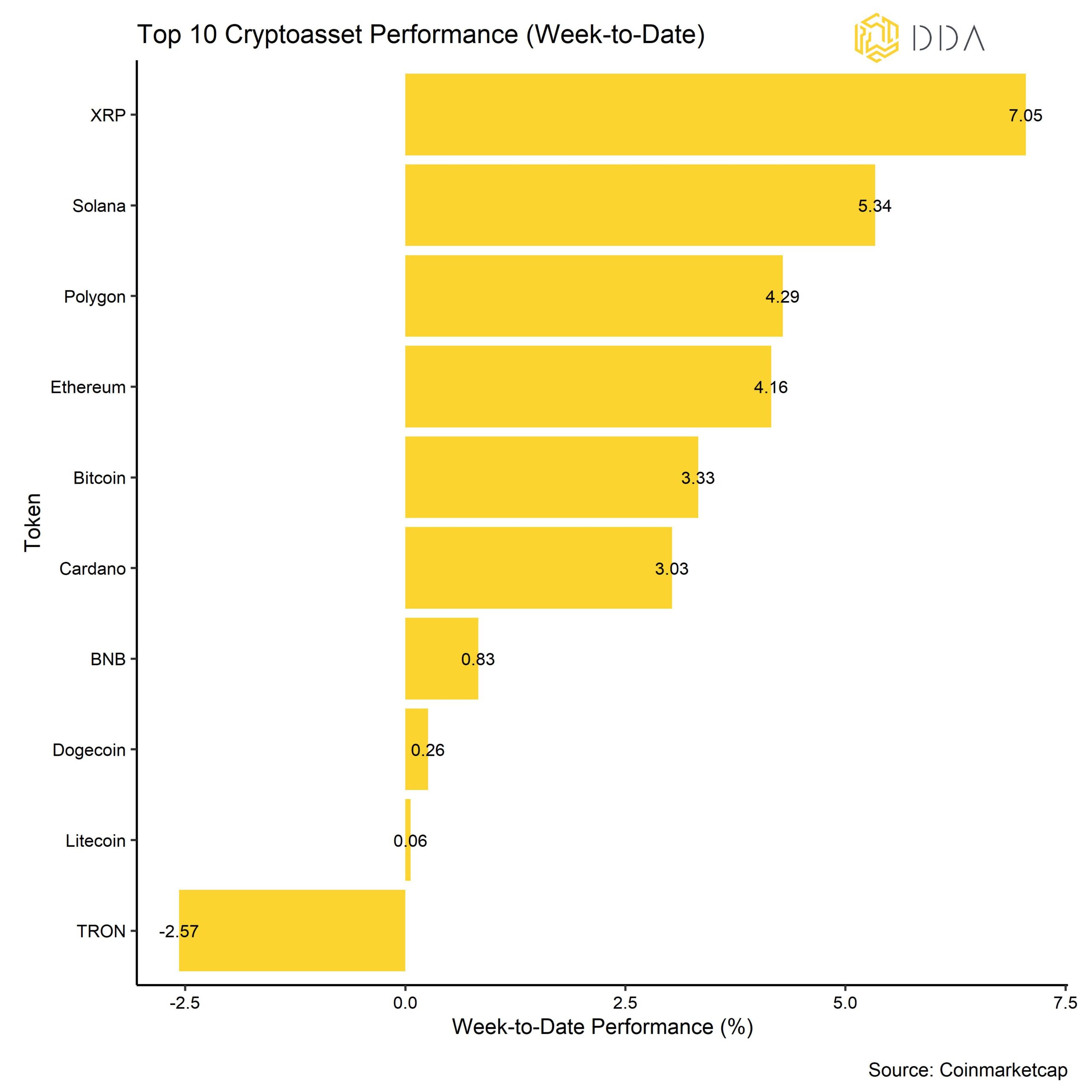

Unter den großen Kryptoassets waren Polygon, Cardano und Solana die relativen Outperformer. Die Gesamt-Outperformance der Altcoins schwächte sich jedoch in der vergangenen Woche wieder ab, wobei nur 35% der erfassten Altcoins auf wöchentlicher Basis eine Outperformance gegenüber BTC erzielten.

Krypto-Marktstimmung

Unser hauseigener Krypto-Sentiment-Index ist weiter gestiegen. 10 von 15 Indikatoren liegen über ihrem kurzfristigen Trend.

Im Vergleich zur letzten Woche gab es große Umschwünge beim Hedgefonds-Bitcoin-Beta und beim 3-Monats-Basissatz des BTC-Futures.

Der Crypto Fear & Greed Index ist im Vergleich zur letzten Woche weitgehend unverändert geblieben und befindet sich heute Morgen immer noch im "neutralen" Bereich.

Die Leistungsstreuung zwischen den Kryptoassets hat in letzter Zeit abgenommen, wenn auch von einem hohen Niveau aus, da die Korrelationen zwischen den Kryptoassets zugenommen haben, was bedeutet, dass die Kryptoassets mehr nach systematischen Faktoren gehandelt werden. Gleichzeitig hat die Outperformance von Altcoins in der letzten Woche etwas nachgelassen und liegt nun bei 35% Altcoins, die Bitcoin auf wöchentlicher Basis übertreffen.

Im Allgemeinen geht die Outperformance von Altcoins mit einer zunehmenden Streuung der Kryptowährungen einher, d. h. Bitcoin und Altcoins werden während der "Altsaison" in der Regel höher gehandelt als Bitcoin, wobei sich Altcoins besser entwickeln als Bitcoin. Eine breitere Outperformance von Altcoins ist in der Regel ein Zeichen für eine zunehmende Risikobereitschaft.

Krypto Asset Flows

In der vergangenen Woche gab es erneut erhebliche Nettoabflüsse aus Kryptoanlagen.

Insgesamt verzeichneten wir Netto-Fondsabflüsse in Höhe von -56,1 Mio. USD (Woche bis Freitag). Allerdings waren die Abflüsse in der vergangenen Woche gleichmäßiger auf die verschiedenen Kryptoassets verteilt und konzentrierten sich nicht nur auf BTC. Bitcoin-Fonds verzeichneten Nettoabflüsse von -18,9 Mio. USD, die meisten davon am vergangenen Freitag. Ethereum-Fonds verzeichneten ebenfalls erhebliche Nettoabflüsse von -15,3 Mio. USD. Sowohl Altcoin-Fonds ohne Ethereum als auch Basket- und thematische Kryptoasset-Fonds verzeichneten ebenfalls Nettoabflüsse (-7,7 Mio. USD bzw. -14,2 Mio. USD).

Außerdem hat sich der Abschlag auf den Nettoinventarwert des größten Bitcoin-Fonds der Welt - Grayscale Bitcoin Trust (GBTC) - erneut vergrößert, was ebenfalls einige Nettoabflüsse aus diesem Fondsvehikel bedeutet.

In der Zwischenzeit ist das Beta der globalen Hedge-Fonds gegenüber Bitcoin in den letzten 20 Handelstagen erneut gestiegen, wenn auch von einem niedrigen Niveau aus, was bedeutet, dass die globalen Hedge-Fonds ihr Engagement in Krypto-Assets erhöht haben. Allerdings ist das Beta noch zu gering, um es als statistisch signifikant zu betrachten. Globale Hedge-Fonds scheinen derzeit im Allgemeinen neutral gegenüber Kryptoassets positioniert zu sein.

On-Chain Tätigkeit

In der vergangenen Woche erholten sich die zentralen On-Chain-Kennzahlen für Bitcoin wie neue oder aktive Adressen größtenteils von den niedrigen Niveaus, die wir aufgrund der Überlastung des Bitcoin-Netzwerks gesehen hatten, die die Netzwerkbeteiligung zum Stillstand gebracht hatte.

Während einige On-Chain-Analysten die sehr geringe Marktliquidität auf der Grundlage von Überweisungen zu und von Börsen als erhebliches Abwärtsrisiko bezeichnen, scheinen größere institutionelle Käufer von Bitcoin die Preise zu drücken, wie die erheblichen Nettoabflüsse von großen Wallets in letzter Zeit zeigen (Chart-der-Woche).

Börsenabflüsse werden als zunehmender Kaufdruck interpretiert, da vor allem größere Investoren ihre Münzen in der Regel von der Börse nehmen, um sie in einem "Kühlhaus" zu lagern.

Am vergangenen Dienstag (25.5.23) gab es den größten Abfluss von mehr als 10 Mio. USD, gemessen an der Größe der Geldbörse.

Im Allgemeinen ist der Grad der Akkumulationsaktivität in den verschiedenen Wallet-Kohorten sehr hoch, insbesondere bei sehr kleinen Kohorten (bis zu 1 BTC) und sehr großen Kohorten (100 bis 100k BTC). Tatsächlich bewegt sich unser durchschnittlicher Akkumulationswert über alle Wallet-Kohorten hinweg immer noch auf dem höchsten Niveau, das wir zuletzt im Jahr 2017 gesehen haben.

Wir gehen davon aus, dass dies zumindest einen Boden unter den aktuellen Preisen bilden wird, und glauben, dass die Abwärtsrisiken aufgrund der sich erholenden Netzaktivität vorerst begrenzt sind.

Ähnlich verhält es sich mit den Umtauschsalden für Ethereum, die weiterhin negative Nettoumtauschströme aufweisen, was ebenfalls ein positives Zeichen ist. Die Netto-Emissionsrate für Ethereum ist mit -1,77% p.a. immer noch negativ/deflationär. Sie hatte am 5.5.2023 aufgrund einer sehr hohen Netzwerkaktivität ein Mehrjahrestief von -8,36% p.a. erreicht und ist seitdem wieder gestiegen.

Während die Anzahl der Transaktionen und aktiven Adressen auf der Ethereum-Blockchain relativ niedrig bleibt, steigen die internen Smart-Contract-Aufrufe deutlich an. Dies unterstreicht die steigende Netzwerkaktivität bei Layer-2-Token, die auf Ethereum basieren.

Krypto-Asset-Derivate

In der letzten Woche sind die impliziten Volatilitäten trotz der seitwärts gerichteten Kursentwicklung weiter gesunken. Der DVOL-Index von Deribit, der die impliziten Volatilitäten von Bitcoin-Optionskontrakten mit einer Laufzeit von 1 Monat abbildet, wird immer noch in der Nähe der im Januar 2023 markierten Tiefststände gehandelt. Die 1-Monats-25-Delta-Optionsschere ist derzeit neutral in Bezug auf die impliziten Volatilitäten.

Nach dem jüngsten Kursanstieg ist das offene Interesse an Put-Call-Positionen leicht gestiegen, während das Verhältnis zwischen Put- und Call-Volumen nach wie vor recht gedämpft ist.

Auf der anderen Seite sind die offenen Positionen in Futures und Perpetual Open Interest gestiegen, da der annualisierte 3-Monats-Basissatz für BTC-Futures ebenfalls leicht gestiegen ist.

Unterm Strich

Vor dem Erlass der Schuldenobergrenze, der vorerst als positiver Katalysator zu wirken scheint, bewegten sich die Kryptoasset-Preise überwiegend seitwärts.

Unser hauseigener Crypto Sentiment Index ist in der vergangenen Woche erneut gestiegen.

Einige institutionelle Käufer von Bitcoin scheinen die Preise zu drücken, wie die erheblichen Abflüsse in letzter Zeit zeigen.

Über DDA Deutsche Digital Assets

Deutsche Digital Assets (DDA) ist ein deutscher Digital Asset Manager, der als vertrauenswürdige Anlaufstelle für Investoren dient, die ein Exposure zu Krypto Assets suchen. Über verschiedene Tochtergesellschaften bietet DDA eine Reihe von kryptobezogenen Anlageprodukten an, die von passiven bis hin zu aktiv verwalteten Investmentlösungen reichen. Darüber hinaus bietet das Unternehmen professionelle Anlageberatung für Family Offices, High Net Worth Individuals (HNWI) und institutionelle Anleger an.

Wir bieten hervorragende Leistungen durch vertraute, vertrauenswürdige Anlagevehikel, die den Anlegern die Qualitätsgarantien bieten, die sie von einem erstklassigen Vermögensverwalter verdienen, während wir uns für unsere Mission einsetzen, die Akzeptanz von Kryptoanlagen zu fördern. DDA beseitigt die technischen Risiken von Krypto-Investitionen, indem wir Anlegern vertrauenswürdige und vertraute Mittel zur Investition in Krypto zu branchenführend niedrigen Kosten anbieten.

Haftungsausschluss

Die in diesem Artikel enthaltenen Materialien und Informationen dienen ausschließlich zu Informationszwecken. Die Deutsche Digital Assets, ihre verbundenen Unternehmen und Tochtergesellschaften fordern nicht zu Handlungen auf der Grundlage dieses Materials auf. Dieser Artikel ist weder eine Anlageberatung noch eine Empfehlung oder Aufforderung zum Kauf von Wertpapieren. Die Wertentwicklung ist unvorhersehbar. Die Wertentwicklung in der Vergangenheit ist daher kein Hinweis auf die zukünftige Wertentwicklung. Sie erklären sich damit einverstanden, Ihre eigenen Nachforschungen anzustellen und Ihre Sorgfaltspflicht zu erfüllen, bevor Sie eine Anlageentscheidung in Bezug auf die hier besprochenen Wertpapiere oder Anlagemöglichkeiten treffen. Unsere Artikel und Berichte enthalten zukunftsgerichtete Aussagen, Schätzungen, Projektionen und Meinungen. Diese können sich als wesentlich ungenau erweisen und unterliegen erheblichen Risiken und Unwägbarkeiten, die außerhalb der Kontrolle der Deutsche Digital Assets GmbH liegen. Wir gehen davon aus, dass alle hierin enthaltenen Informationen korrekt und zuverlässig sind und aus öffentlichen Quellen stammen. Diese Informationen werden jedoch "wie besehen" und ohne jegliche Garantie präsentiert.