Bitcoin-Saisonalität "Im Mai verkaufen und weggehen?"

von André DragoschLeiter der Forschung

Wichtigste Erkenntnisse

- Historische Bitcoin-Performance-Muster deuten darauf hin, dass die Performance von menschlicher Routine beeinflusst sein könnte, obwohl der Bitcoin 24/7/365 gehandelt wird.

- Es spricht einiges für eine "Sommerflaute" bei Kryptoassets, da Bitcoin historisch gesehen in den Monaten Juni bis September unterdurchschnittliche Renditen aufweist, während April, Mai, Oktober und November historisch gesehen die höchsten durchschnittlichen Renditen aufweisen

- Arbeitstage von Montag bis Mittwoch und die täglichen Handelszeiten in London und New York weisen historisch gesehen eine überdurchschnittliche BTC-Performance auf

Ein altes Wall-Street-Sprichwort besagt: "Sell in May and go away", was bedeutet, dass die Monate nach April in der Regel unterdurchschnittliche Renditen für Aktien aufweisen. Es gibt auch eine umfangreiche akademische Literatur, die darauf hindeutet, dass die Saisonalität eine große Rolle für die Aktienrenditen spielen kann und dass einige Monate wie der Januar in der Vergangenheit deutlich höhere Renditen als andere Monate aufwiesen (so genannter "Januareffekt").

Aber was ist mit Krypto-Assets?

Unter Verwendung aller verfügbaren Preisdaten für Bitcoin haben wir die monatlichen, täglichen und sogar stündlichen Performance-Muster im Laufe der Zeit analysiert.

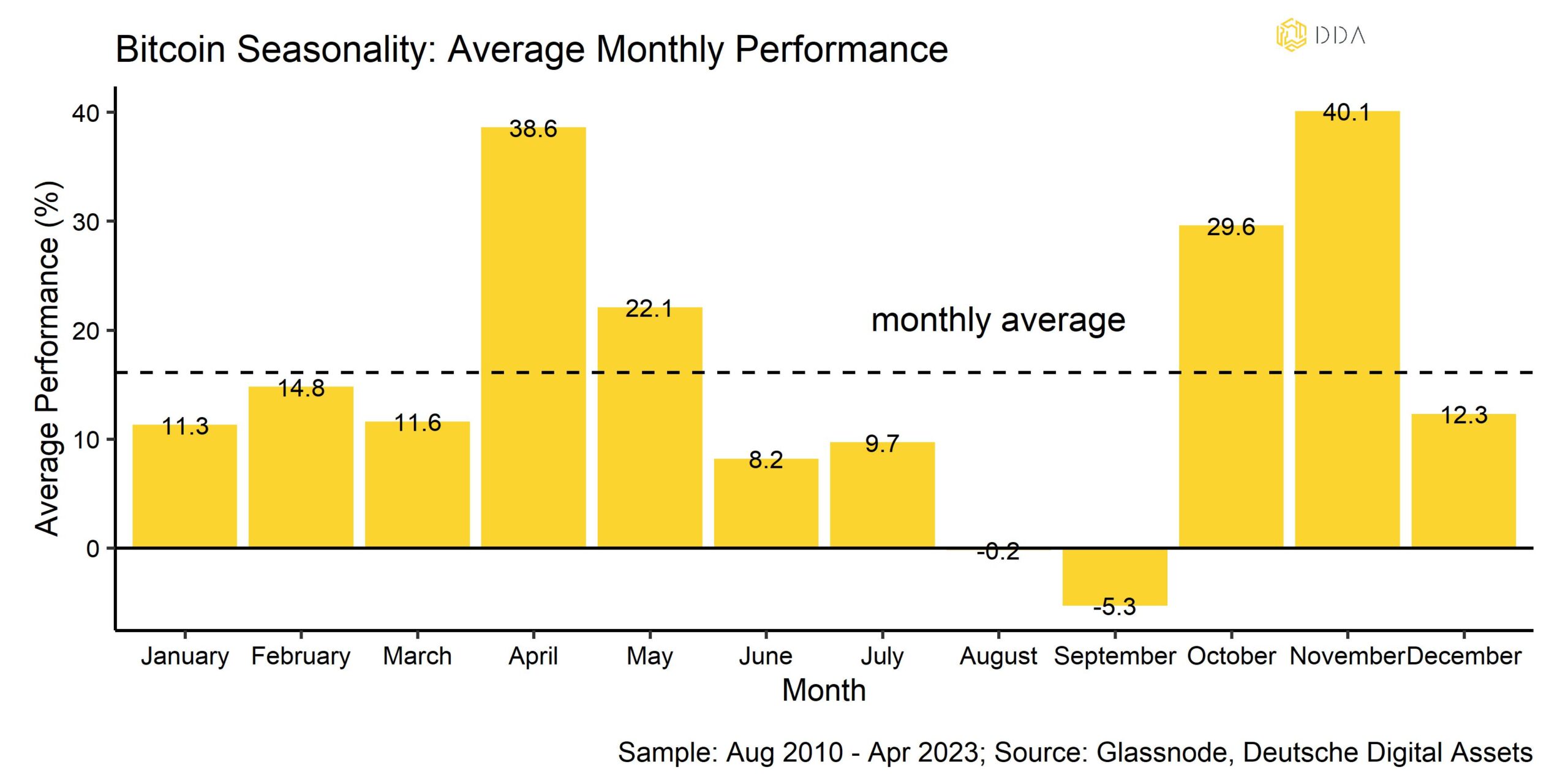

Das obige Diagramm zeigt beispielsweise die durchschnittliche monatliche Performance von Januar bis Dezember, seit BTC/USD-Preisdaten verfügbar sind. Die Ergebnisse deuten darauf hin, dass der Monat Mai seit 2011 im Durchschnitt eine überdurchschnittliche Rendite von 22,1% aufweist. Im Allgemeinen waren die Monate April, Mai, Oktober und November historisch gesehen die besten Monate, um Bitcoin zu halten.

Im Gegensatz dazu haben die Monate Juni bis September in der Vergangenheit die schwächste Bitcoin-Performance gezeigt. Es spricht also einiges für eine "Sommerflaute" bei Kryptoassets, insbesondere bei Bitcoin. Generell legen die Ergebnisse nahe, dass Kryptoasset-Anleger ihre Bitcoin-Positionen zumindest bis Juni halten und "Ende Mai verkaufen" sollten.

So könnte beispielsweise eine einfache Handelsregel das BTC-Engagement vor Beginn der Sommermonate von Juni bis September reduzieren, aber das Engagement in den Monaten von Oktober bis Mai wieder erhöhen.

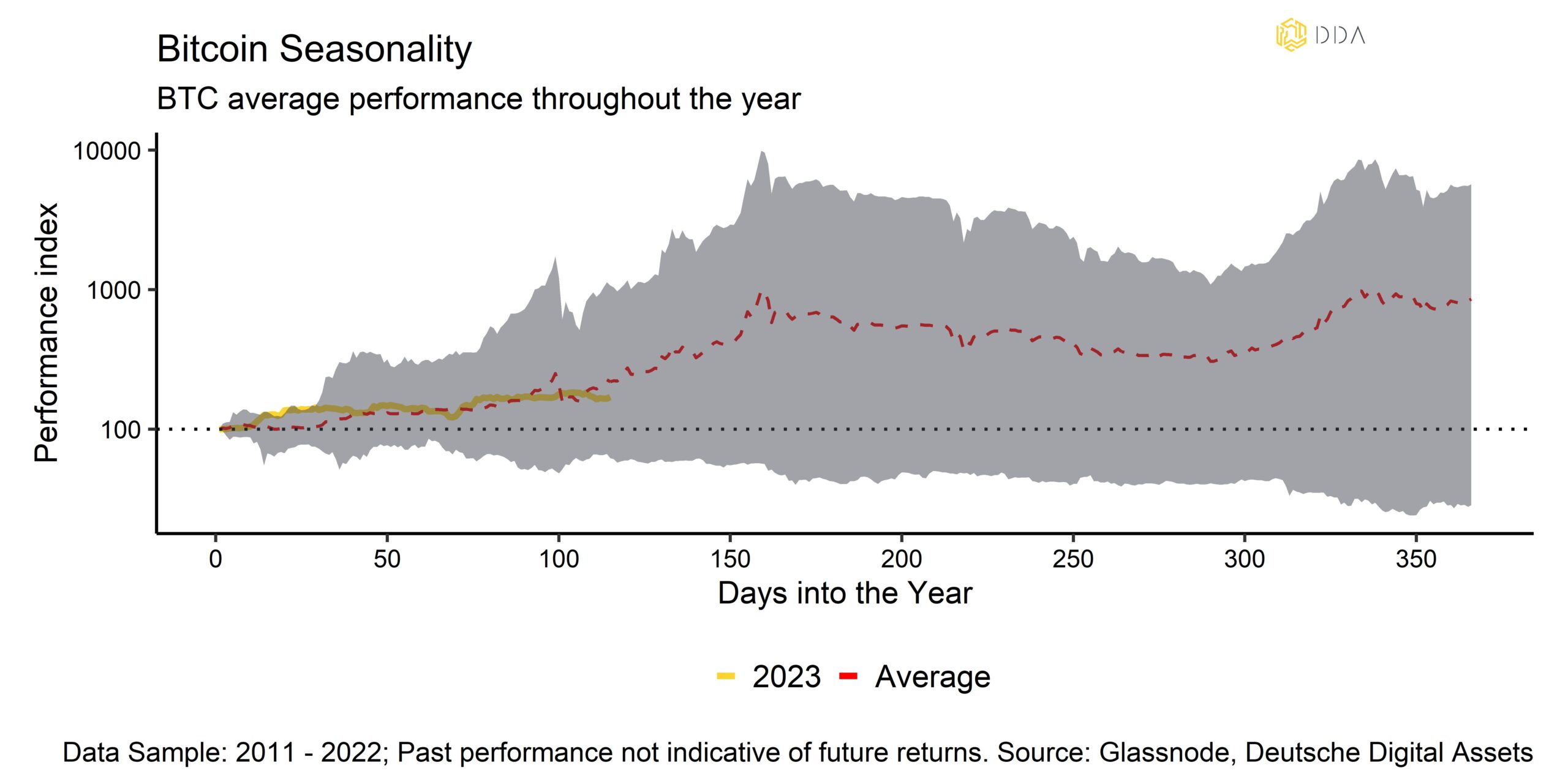

Dies wird auch in der folgenden Grafik deutlich, die die durchschnittliche und die jeweilige minimale und maximale Performance von Bitcoins im Laufe des Jahres zeigt:

Bislang folgt die Entwicklung von Bitcoin ziemlich genau den historischen Performance-Mustern und lässt kurzfristig noch etwas mehr Aufwärtspotenzial erwarten, bevor er sich seitwärts zu bewegen beginnt.

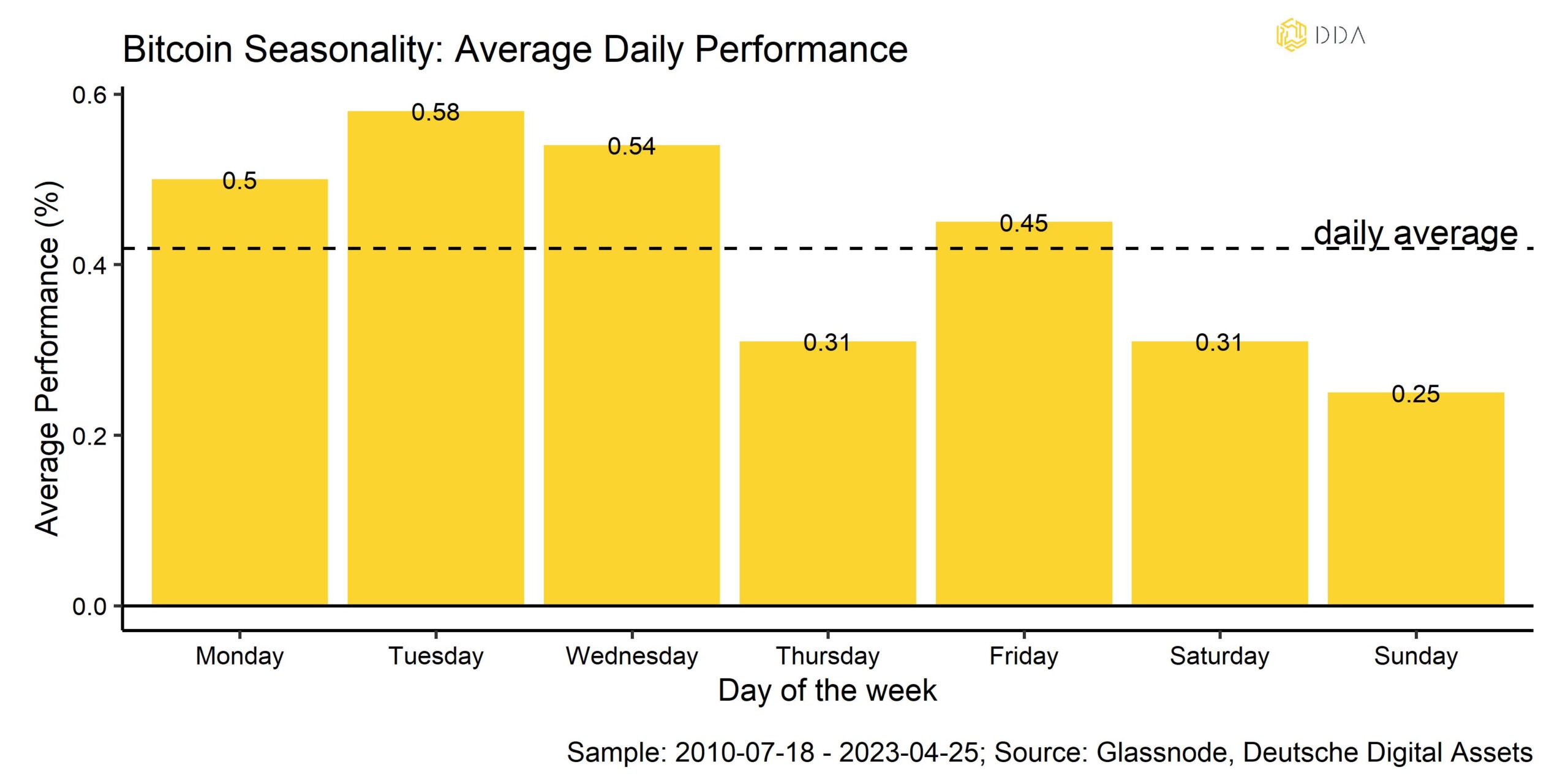

Betrachtet man die täglichen Daten, so haben Wochentage zu Beginn der Woche wie Montag bis Mittwoch in der Vergangenheit überdurchschnittliche Renditen für Bitcoin gezeigt, während Donnerstage und Wochenenden unterdurchschnittliche Renditen aufwiesen.

Die täglichen Performance-Muster deuten also darauf hin, dass die menschliche Routine (Arbeit von Montag bis Freitag und Urlaub am Wochenende) auch die Bitcoin-Renditen beeinflussen könnte.

Eine einfache Handelsregel könnte beispielsweise dieses Performance-Muster ausnutzen, indem das BTC-Engagement vor Wochenbeginn erhöht und danach, insbesondere vor Wochenenden, reduziert wird.

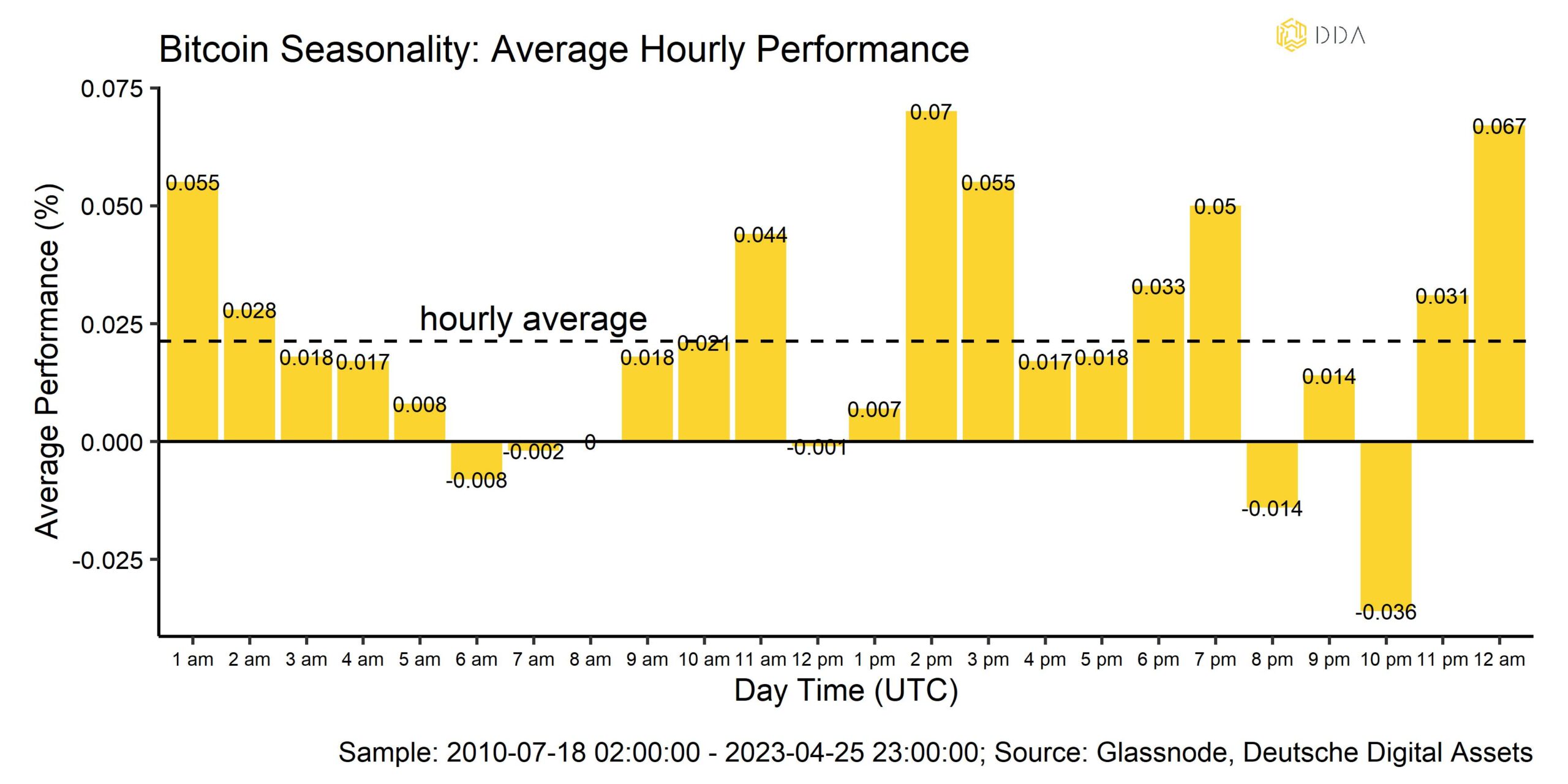

In diesem Zusammenhang ist es interessant zu beobachten, dass die täglichen Devisenhandelszeiten in London (7.00 - 16.00 Uhr) und New York (13.00 - 22.00 Uhr) in der Vergangenheit auch für Bitcoin überdurchschnittliche Renditen aufwiesen, während die Handelszeiten in Tokio (1.00 - 9.00 Uhr) unterdurchschnittliche Renditen erbrachten.

So könnte beispielsweise eine einfache Handelsregel das BTC-Engagement vor den Handelszeiten in London und New York erhöhen und während der Handelszeiten in Tokio ("über Nacht") verringern.

Alles in allem deuten die Ergebnisse darauf hin, dass die Bitcoin-Performance trotz der Tatsache, dass Bitcoin rund um die Uhr gehandelt wird, durch menschliche Routine beeinflusst worden sein könnte.

Im Allgemeinen sollten Kryptoasset-Investoren auf der Grundlage dieser Ergebnisse tatsächlich "verkaufen [Ende Mai] und verschwinden".

"Aber denken Sie daran, im September wiederzukommen", wie ein altes Sprichwort besagt.

Wie immer hoffen wir, dass diese Erkenntnisse für Sie nützlich sind.

Bleiben Sie bescheiden und stapeln Sie Sats,

André

Registrieren Sie sich für den DDA-Newsletter hier und erhalten Sie unsere neuesten Forschungsberichte, wöchentliche Marktanalysen und die neuesten Erkenntnisse über Makro-, Industrie- und Kryptomarkttrends von unseren Top-Experten direkt in Ihren Posteingang.

Haftungsausschluss

Die in diesem Artikel enthaltenen Materialien und Informationen dienen ausschließlich zu Informationszwecken. Die Deutsche Digital Assets, ihre verbundenen Unternehmen und Tochtergesellschaften fordern nicht zu Handlungen auf der Grundlage dieses Materials auf. Dieser Artikel ist weder eine Anlageberatung noch eine Empfehlung oder Aufforderung zum Kauf von Wertpapieren. Die Wertentwicklung ist unvorhersehbar. Die Wertentwicklung in der Vergangenheit ist daher kein Hinweis auf die zukünftige Wertentwicklung. Sie erklären sich damit einverstanden, Ihre eigenen Nachforschungen anzustellen und Ihre Sorgfaltspflicht zu erfüllen, bevor Sie eine Anlageentscheidung in Bezug auf die hier besprochenen Wertpapiere oder Anlagemöglichkeiten treffen. Unsere Artikel und Berichte enthalten zukunftsgerichtete Aussagen, Schätzungen, Projektionen und Meinungen. Diese können sich als wesentlich ungenau erweisen und unterliegen erheblichen Risiken und Unwägbarkeiten, die außerhalb der Kontrolle der Deutsche Digital Assets GmbH liegen. Wir gehen davon aus, dass alle hierin enthaltenen Informationen korrekt und zuverlässig sind und aus öffentlichen Quellen stammen. Diese Informationen werden jedoch "wie besehen" und ohne jegliche Garantie präsentiert.