KEY TAKEAWAYS

- STRC’s troubles are a corporate balance-sheet and liquidity story, not a Bitcoin protocol story — blocks keep getting mined on schedule regardless of any single company’s capital structure.

- The real, near-term risk is mechanical: as Bitcoin’s price falls, Strategy’s dividend-funding cushion shrinks, forcing larger BTC sales to cover STRC’s fixed cash payout — exactly what has been playing out in June 2026.

- Paying the dividend directly in BTC — a model already proven by BTCS Inc. (Nasdaq), which paid a Bitcoin-denominated “Bividend” in 2022 and repeated the structure with an Ethereum dividend in 2025 — would remove the forced-selling mechanism, though it carries its own trade-offs for a product marketed as short-duration yield.

What STRC actually is

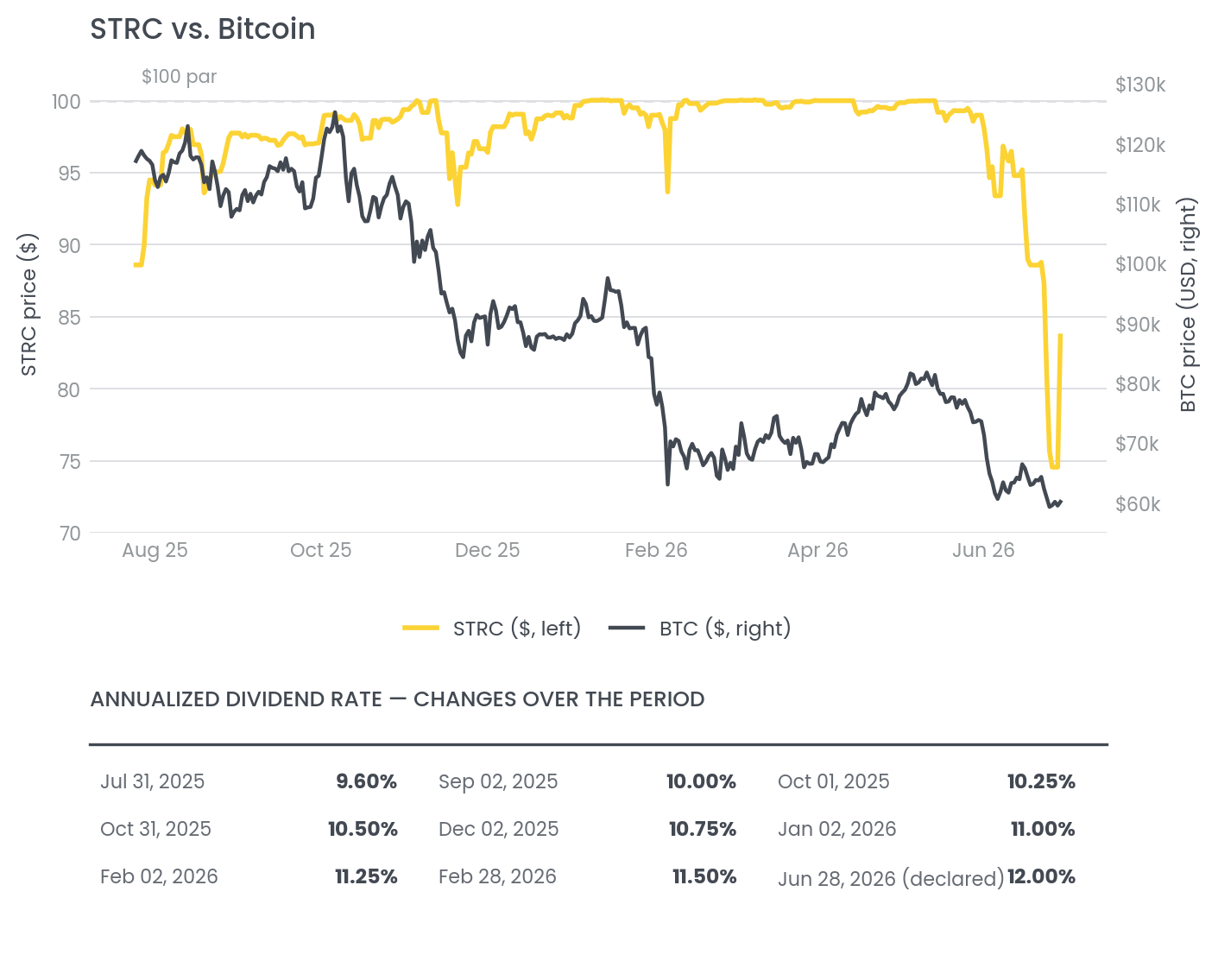

Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock (STRC, Nasdaq) is a perpetual preferred share with no maturity date, designed to trade near its $100 par value. Its annualized dividend rate is adjusted monthly — currently 12.00% effective for July 2026 record dates, up from 11.50%, after STRC traded as low as $71-75 in late June as Bitcoin fell below $60,000. Notional outstanding stands at roughly $10.5 billion. STRC ranks ahead of common shareholders (MSTR) for dividends and liquidation claims, but it is not collateralized by Strategy’s bitcoin holdings — it only carries a general preferred claim on residual assets.

Strategy itself holds approximately 845,000–847,000 BTC (roughly 4% of total supply), and has recently paused further accumulation, instead building a ~$2.55 billion USD reserve and announcing a $1 billion digital credit buyback program — a sign that capital allocation is shifting toward shoring up the balance sheet rather than continued buying.

The ‘systemic risk’ claim

As STRC fell well below the $100 par value, a vocal corner of the market began framing the situation as a systemic risk to Bitcoin itself: forced BTC selling to fund dividends, a depeg of STRC, and a feedback loop sometimes described as a ‘death spiral’ for Strategy’s flywheel. Some commentary goes further, framing this as proof that public equities are an inherently dangerous proxy for crypto exposure.

Other analysts have pushed back specifically on the systemic framing. K33’s research has noted the structure does not currently pose an immediate systemic risk to BTC, citing Strategy’s cash cushion, even while flagging structural risks tied to sentiment and pricing dynamics. CryptoQuant analysis has likewise pointed to four real pressures on Strategy — Bitcoin trading below its average cost basis, STRC’s declining financing capacity, BTC sales undercutting the ‘buy-only’ narrative, and equity dilution — while concluding there is no systemic risk in the short term.

Why we disagree with the ‘systemic risk to Bitcoin’ framing

We agree with the more measured analysts on the core point: this is not an existential risk to Bitcoin. Bitcoin’s issuance schedule, security, and settlement do not depend on any single holder’s solvency — not Strategy’s, not any other treasury company’s. Even in a scenario where Strategy were forced to liquidate its entire ~845,000 BTC position, the network would continue producing blocks every ~10 minutes, on schedule, exactly as it has since 2009.

What critics are actually describing is concentration risk and forced-seller risk — real and worth monitoring, but categorically different from a threat to the protocol. A large holder being forced to sell into a falling market can move price, sometimes sharply, but it does not change Bitcoin’s monetary policy, its decentralization, or its long-term scarcity. We also believe such a scenario would – just like prior forced sellers like Terra Luna, FTX, and others – have no impact on Bitcoin’s credibility as a network. Conflating ‘this is bad for one company’s stock and possibly for short-term price action’ with ‘this threatens Bitcoin’s existence’ overstates the case considerably.

The real risk is short-term and mechanical

Where we do think the criticism has merit is on the mechanics of funding the dividend payments for its various outstanding preferred and debt instruments. STRC’s payout is fixed in USD terms (currently 12.00% of $100 par, paid semi-monthly in cash). When Bitcoin’s price falls, the effective ‘reserve’ Strategy can tap — unrealized BTC gains and any USD buffer — shrinks, and the company may need to sell a larger quantity of BTC to raise the same dollar amount. This is precisely the dynamic that pushed Strategy to raise the dividend rate to defend STRC’s par value while simultaneously building a larger USD cash reserve — in effect, pre-funding future dividend payments to reduce reliance on opportunistic BTC sales during weak markets.

This is a liquidity and capital-structure question for Strategy and a risk question for STRC holders (and, to a lesser extent, MSTR common holders, who sit behind STRC in the capital stack). It is not a Bitcoin network risk.

Our view: STRC’s dividend mechanics are a balance-sheet and liquidity risk for Strategy — not a threat to Bitcoin issuance, which keeps running on schedule regardless of any single company’s capital structure. Tick tock, next block — as they say.

Figure 1 — STRC vs. Bitcoin price since STRC’s July 2025 launch, with the annualized dividend rate schedule below. Source: Bloomberg, Deutsche Digital Assets.

An alternative — pay the dividend in BTC

One structural fix worth floating: instead of a fixed USD-denominated cash dividend that forces BTC sales when the price drops, Strategy could pay STRC’s dividend directly in bitcoin. This is not unprecedented — in January 2022, BTCS Inc. (Nasdaq: BTCS) paid out the firstever dividend payable in Bitcoin by a Nasdaq-listed company, a $0.05-per-share “Bividend” that shareholders could elect to receive in BTC or cash. BTCS repeated the structure in 2025 with an Ethereum-denominated dividend, confirming the mechanism works in practice, not just on paper.

Applied to STRC, a BTC-denominated dividend would remove the forced-selling mechanism entirely: Strategy would simply distribute bitcoin pro rata rather than converting it to dollars first. It would also better align the instrument with what it actually is — indirect Bitcoin exposure — rather than disguising it as a fixed-income product.

The trade-off is real, though: STRC is explicitly marketed as ‘short duration high yield credit’ for income-oriented investors who want reduced volatility and a predictable cash payout, not spot BTC exposure with its attendant price swings. A BTC-denominated dividend would solve Strategy’s forced-selling problem but would shift volatility (and potentially tax/accounting complexity) onto income seeking holders who may not want it — likely requiring a different investor base or a hybrid/optional structure rather than a wholesale conversion.

Schlussfolgerung

Strip away the alarmist framing and what’s left is a fairly ordinary corporate finance problem: a company with a large, volatile asset on its balance sheet has issued a fixed-rate cash obligation, and is now managing the mismatch between the two. That is worth watching closely if you hold STRC, MSTR, or any of Strategy’s other preferred instruments — it speaks directly to dividend sustainability and capital-structure risk. It says nothing, however, about whether Bitcoin works. The network doesn’t care who owns 4% of its supply, what their cost basis is, or whether their preferred stock trades at $75 or $100. The question worth asking isn’t ‘is Bitcoin at risk because of STRC?’ — it’s ‘how is Strategy managing its cash?’ Those are very different questions, and conflating them does a disservice to both.

REFERENCES

[1] Strategy — STRC Information page: strategy.com/strc/learn

[2] The Block — “Strategy’s STRC-fueled bitcoin buying spree highlights sentiment-driven structural risks: K33”

[3] The Block — “Strategy pauses bitcoin buys, establishes $1B digital credit repurchase program as USD reserve

tops $2.5B”

[4] KuCoin — “Strategy Death Spiral Debunked: Why MSTR’s Crypto Flywheel Paused as STRC Preferred Stock Hits

$75 Amid Bitcoin Slump”

[5] KuCoin — “STRC Preferred Stock Reaches New Low as Strategy Faces Funding Pressure” (CryptoQuant / Adam

Back commentary)

[6] Bitcoin Magazine Pro — “STRC Explained: How Strategy’s Perpetual Stretch Preferred Stock Works”

[7] OAK Research — “STRC: How Strategy Turned Bitcoin Into a Yield Product”

[8] BTCS Inc. — “BTCS First-ever Nasdaq-listed Company to Offer a Dividend Payable in Bitcoin” (Bividend, January

2022); “BTCS Engages Equity Stock Transfer… First Blockchain Dividend Payable in Ethereum” (August 2025)

[9] BitcoinTreasuries.net / The Block Treasuries — Strategy BTC holdings data

[10] Bloomberg — STRC (EP060888 Pfd) and XBTUSD price history; STRC dividend declaration history (DVD)

Wichtige Hinweise:

The material and information contained in this article is for informational purposes only. Deutsche Digital Assets GmbH, its affiliates, and subsidiaries

are not soliciting any action based upon such material. This article is neither investment advice nor a recommendation or solicitation to buy any

securities. Performance is unpredictable. Past performance is hence not an indication of any future performance. You agree to do your own research

and due diligence before making any investment decision with respect to securities or investment opportunities discussed herein. Our articles and

reports include forward-looking statements, estimates, projections, and opinions. These may prove to be substantially inaccurate and are inherently

subject to significant risks and uncertainties beyond Deutsche Digital Assets’ control. We believe all information contained herein is accurate, reliable

and has been obtained from public sources. However, such information is presented “as is” without warranty of any kind.

This article represents solely a non-binding preliminary information which serves exclusively advertising purposes. It is not a prospectus in the sense

of the Regulation (EU) 2017/1129 (Prospectus Regulation) and the German Securities Prospectus Act (Wertpapierprospektgesetz – WpPG).

Risikoerwägungen:

The price of an investment in a DDA ETP may go up or down and the investor may not get back the amount invested. The price performance of

cryptocurrencies is highly volatile and unpredictable. Past performance is hence no guarantee of future performance. You agree to do your own

research and due diligence before making any investment decision with respect to securities or investment opportunities discussed herein. The

approval of the prospectus should not be construed as an endorsement of the securities offered or admitted to trading on a Regulated Market. These

are not extensive risk considerations. Prospective investors should read the prospectus before making any investment decision in order to fully

understand the potential risks and rewards of deciding to invest in the securities. The prospectus of each ETP product is available at DDA Crypto ETPs –

Deutsche Digital Assets.

Securities issued by DDA Europe GmbH, DDA ETP GmbH, DDA ETP AG or any other issuer have not been registered under the U.S. Securities Act of 1933,

as amended, (the “Securities Act”). The notes are being offered outside the United States of America (the “United States” or “U.S.”) in accordance with

Regulation S under the Securities Act (“Regulation S”), and may not be offered, sold or delivered within the United States except pursuant to an

exemption from, or in a transaction not subject to, the registration requirements of the Securities Act. The information provided on this website is not

directed to any United States person or legal entity or any state thereof, or any of its territories or possessions. U.S. PERSONS (AS DEFINED IN REGULATION

S) AND LEGAL ENTITIES RESIDENT IN THE UNITED STATES MAY NOT ENTER THIS WEBSITE. Information from this website may not be distributed or

redistributed into the United States or into any jurisdiction where it is not permitted.

@Deutsche Digital Assets │2026│ DDA Crypto Espresso : STRC Isn’t a Bitcoin Problem — It’s a Strategy Problem